Earnings on Ice, Valuations on Fire: A Market Built on Thin Air?

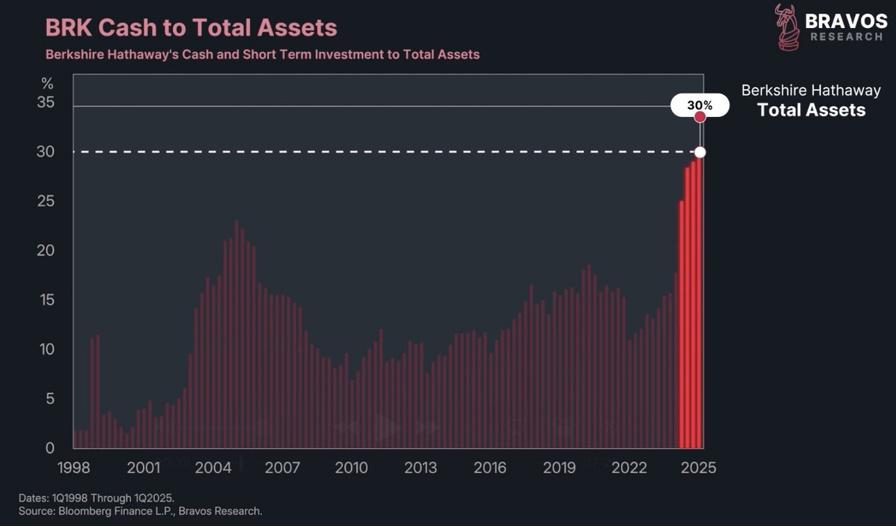

Warren Buffett’s Berkshire Hathaway has once again raised its cash holdings to nearly 30% of total assets, a level historically seen only ahead of major economic downturns. This mirrors past episodes such as:

- The Dot-com Bubble(2000)

- The Global Financial Crisis(2008)

- The Covid Crash(2020)

Each time this kind of cash pile built up, it preceded a significant market dislocation.

Warren Buffett’s cautious stance is borne out by the fact that stock prices have surged far ahead of earnings growth, highlighting a growing disconnect between market optimism and underlying fundamentals.

This signals investors are betting on future growth far beyond what analysts or corporate earnings currently justify.

This second chart starkly illustrates the disconnect:

- The MSCI ACWI Index price has surged nearly 30% since early 2024

- Meanwhile, forward earnings expectations have only risen modestly (13%)

Such a wide divergence between price and earnings growth has historically preceded market corrections. It suggests a high degree of speculation and complacency, much like the late stages of previous bull markets.

Putting both charts together, the message is unambiguous:

- Smart money is on defense (Buffett’s cash hoarding)

- Retail/institutional sentiment is chasing momentum (equity surge vs. EPS lag)

This contrast heightens the risk of a macro reversion event where either corporate earnings must accelerate sharply to justify elevated equity prices (a low-probability outcome), or valuations will be forced to correct downward (a higher-probability scenario), especially if global economic growth continues to weaken.

Conclusion

The current rally in global equities is increasingly driven by sentiment and liquidity, rather than underlying earnings strength. The sharp divergence between price gains and forward EPS suggests markets are overpricing growth optimism.

At the same time, Buffett’s near-record cash levels signal caution from seasoned investors, typically a precursor to market stress.

Recent tariff saga, policy uncertainty, and weakening investment data globally suggest we are in a late-cycle environment. Markets may remain elevated in the short term, but the risk-reward looks increasingly asymmetric.

We remain cautious on risk assets and expect higher volatility and potential downside unless macro data or earnings meaningfully improve.

Comments are closed.