Echoes of 2000, Lessons for 2025: The Rise of Tech and Fall of Safety

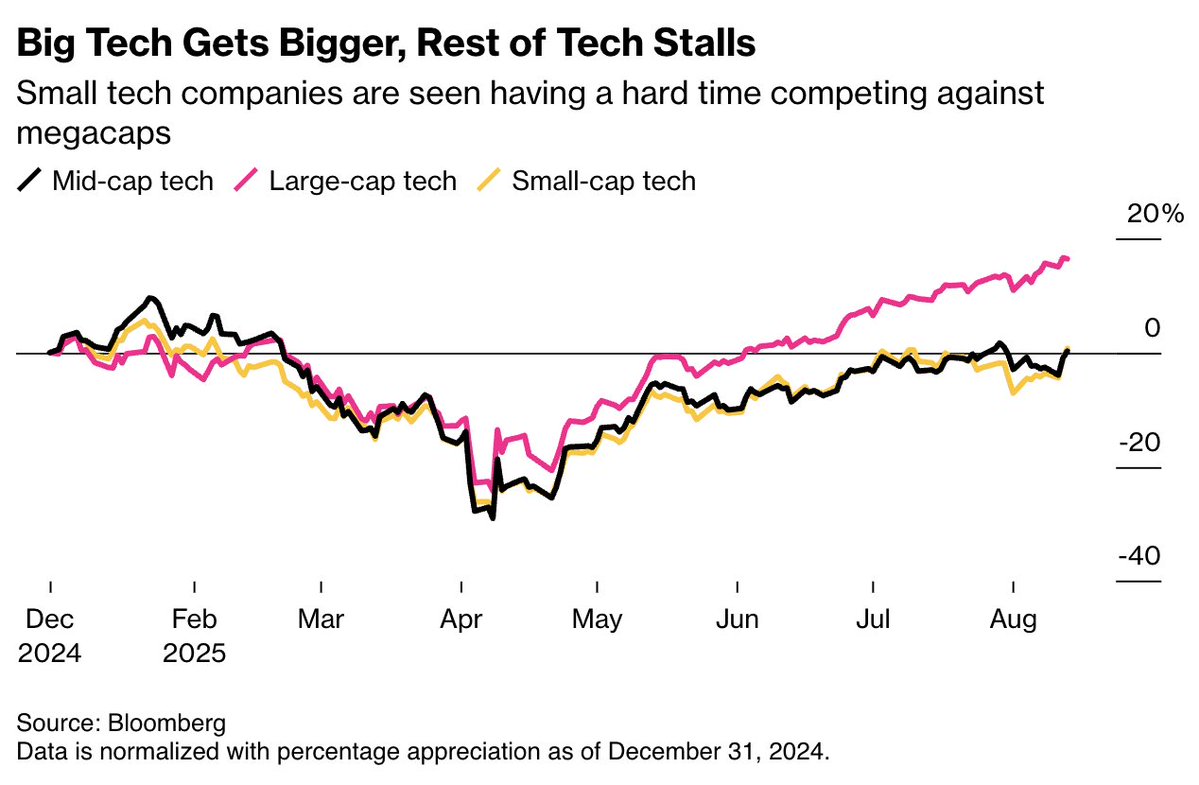

The above chart shows how the market is paying up for growth, with large-cap tech delivering a +16% surge year-to-date, compared with a –1% decline in small-cap tech and flat performance for mid-cap peers. The message is clear: investors see superior earnings visibility, stronger balance sheets, and AI-led growth in the giants, while smaller firms are being penalized for weaker funding access and limited competitive edge.

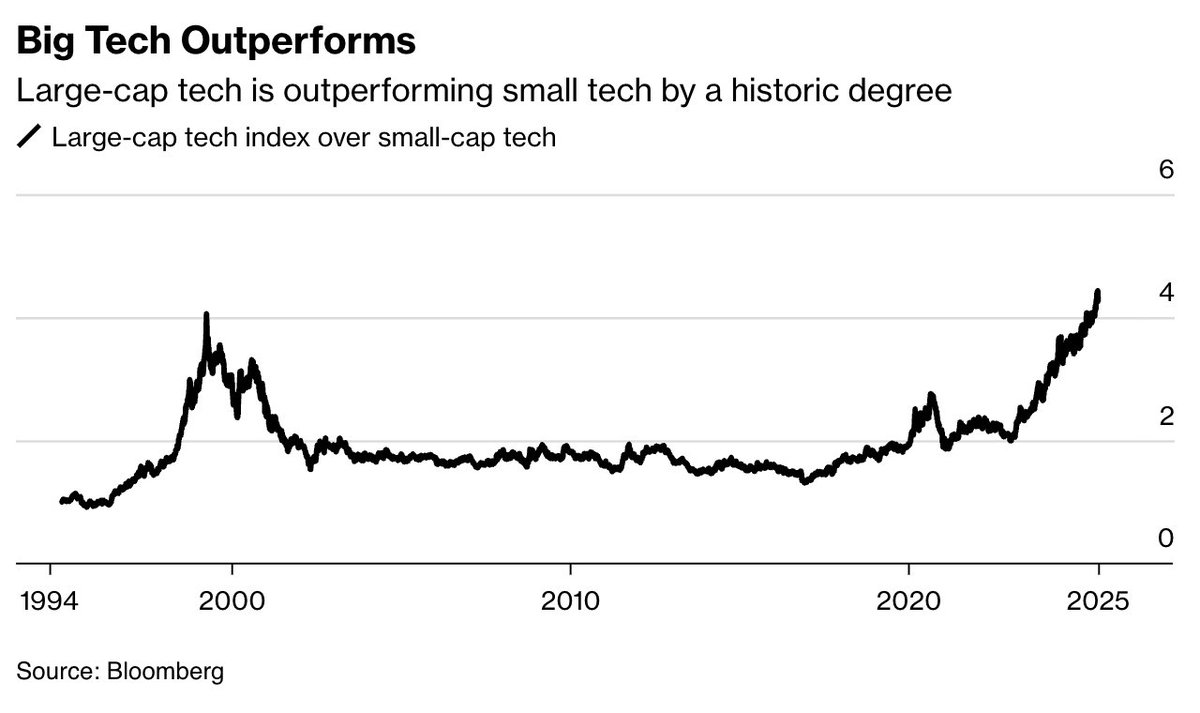

If we look at this second chart, the picture becomes even clearer. The relative performance spread between large-cap and small-cap tech has blown out to the widest margin in over 30 years, even eclipsing the extremes of the Dot-Com era. What began as a simple performance gap (Chart 1) has now compounded into a historic divergence in relative strength, underscoring how scale and market leadership are being disproportionately rewarded in this cycle.

Unlike past cycles, today’s divergence is reinforced by AI-driven investment intensity, global capital concentration, and the strong balance-sheetmega caps. These structural advantages make it possible that large-cap dominance could persist for longer than historical precedent, even as risks of over-concentration build beneath the surface.

Conclusion

We believe this widening gulf between large-cap and small/mid-cap tech reflects both structural tailwinds (AI adoption, scale economics, global reach) and cyclical headwinds (higher funding costs, weak capital access for smaller firms). While mega cap leadership looks justified near term, history shows that periods of extreme concentration rarely sustain indefinitely without sharp corrections.

Today, concentration risk is building, with index performance increasingly dependent on a narrow group of dominant firms. This trend may continue as long asthe second and third delta of innovation cycles favor the leaders, but the risk-reward has become increasingly asymmetric. A prudent approach is to stay aligned with large-cap momentum in the short term while simultaneously preparing for mean-reversion opportunities in the medium to long term.

Comments are closed.