EM Rally Looks Stretched: A Turning Point Ahead?

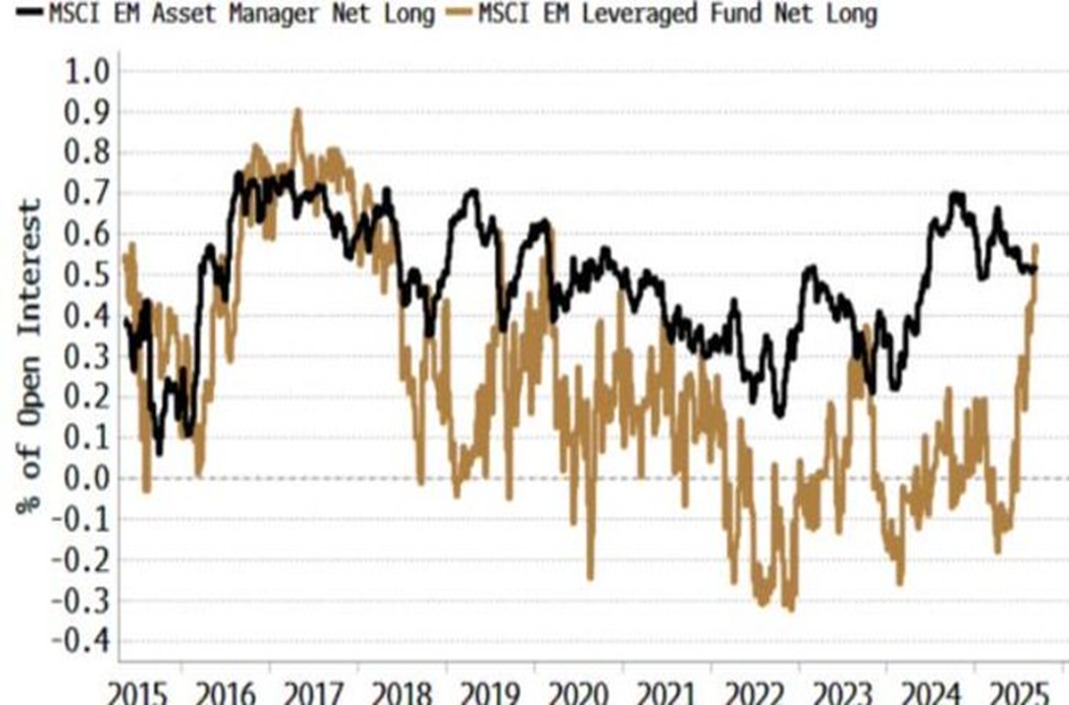

This first chart shows the positioning of asset managers (black) and leveraged funds (brown) in MSCI Emerging Markets futures. While asset manager positioning tends to be more stable and reflective of long-term allocations, the leveraged fund line reflects “fast money” hedge funds and tactical players. What stands out is the sharp acceleration higher in 2025: leveraged funds have rapidly built long positions, signaling strong speculative conviction in an EM rally.

Historically, these surges of leveraged fund longs in EM assets have coincided with periods of dollar weakness, improving global liquidity, and stronger relative growth in emerging economies. In other words, hedge funds are positioning aggressively for a pro-EM cycle, with equities in focus.

This second chart illustrates speculative positioning in the dollar, broken down between developed market (DM) FX and emerging market (EM) FX. The white line shows speculators’ net dollar position versus DM currencies, which remains close to flat. The blue line, however, shows speculators heavily short the dollar against EM FX, meaning they are long EM currencies.

The divergence is striking: speculators are not betting on a weaker dollar against G10 currencies, but they are positioning strongly for EM FX appreciation versus the USD. This suggests that investors see relative out performance coming specifically from emerging markets, rather than broad-based global dollar weakness.

Together, the charts tell a coherent story: speculative capital is simultaneously buying EM equities and EM currencies. This alignment suggests investors expect a period of USD softness, Fed easing, and stronger relative EM growth, drawing capital flows into higher-yielding and higher-beta assets.

Implications

The current configuration of flows leaves EM assets vulnerable. With leveraged funds heavily long, any change in global risk appetite could trigger rapid unwinds, magnifying downside in both EM equities and FX.

U.S. resilience is a key risk. Stronger growth or sticky inflation could revive Fed hawkishness, strengthen the dollar, and reverse EM currency gains.

Commodities, which have benefited from EM demand and dollar softness, would also be at risk if EM FX weakens and import demand slows.

On equities, relative performance could tilt back toward the U.S., where earnings growth is more insulated. This would leave EM markets struggling to justify stretched positioning despite cheaper valuations.

Conclusion

The synchronized surge into EM equities and EM FX marks a late-cycle extension of the pro-EM trade. While momentum could persist in the near term, speculative positioning is already extreme. This raises the likelihood of under performance in EM assets relative to the U.S. in the months ahead.

In short, what began as a broad EM opportunity now looks stretched: investors should be cautious of chasing the trade further, as risks of reversal are building.

Comments are closed.