How Rising Household Debt Is Reshaping India’s Macro Landscape

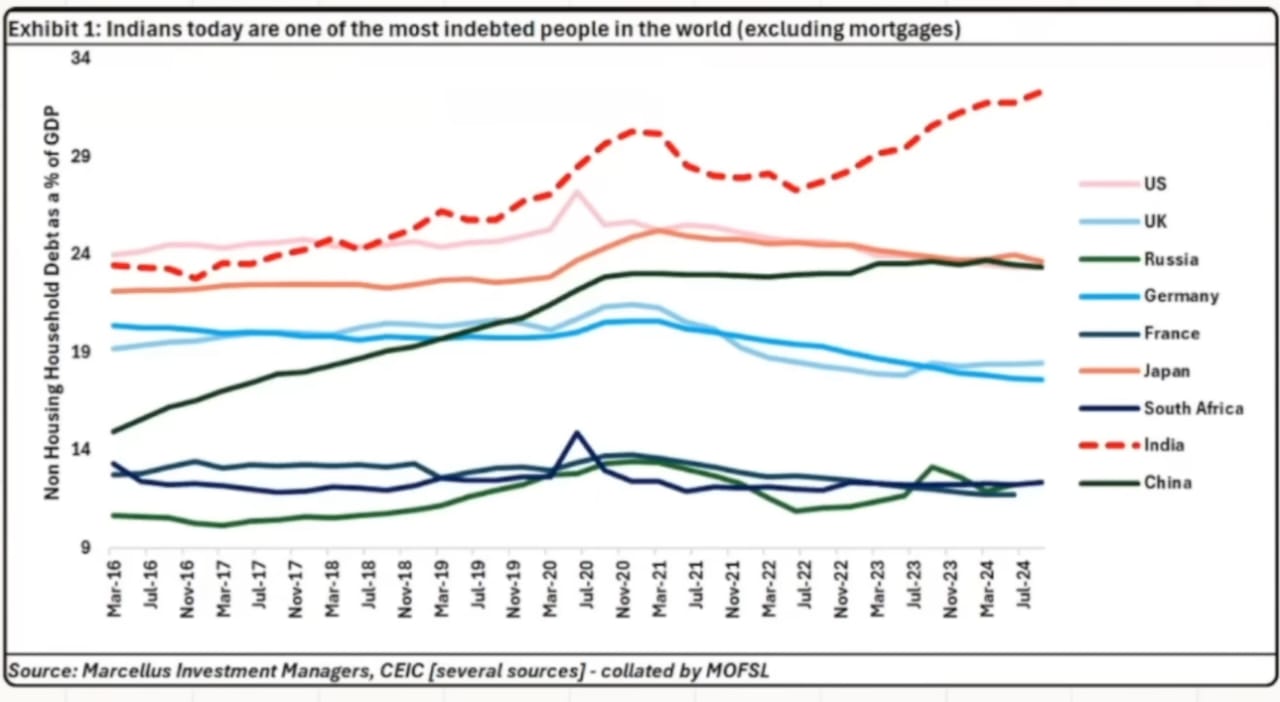

This chart highlights India’s sharp build-up in non-housing household debt, which has climbed to over 29% of GDP, making Indian households among the most leveraged globally (excluding mortgages). The ratio now exceeds those of the US, UK, France, Germany, and Japan, and remains significantly above China and Russia, both under 17%.

The upward trend since 2016 reflects a structural shift in household behavior from savings-led consumption to credit-fueled spending. Easy access to unsecured loans, personal credit lines, and consumer finance has supported robust demand in sectors like autos, electronics, and services. However, this growing dependence on unsecured borrowing raises concerns about financial fragility if income growth falters or interest rates remain elevated.

India’s debt build-up is consumption-driven rather than asset-backed, which magnifies the risk of demand compression and delinquencies in a slowdown. The trend underscores a key macro trade-off: while household credit deepens financial inclusion and boosts short-term GDP, it can amplify vulnerabilities across the financial system.

Macro Impact

- GDP and Consumption

Rising household leverage has been a short-term tailwind for GDP, powering consumption-led growth, which contributes nearly 60% to India’s economy. However, as debt-servicing costs absorb a larger share of disposable income, the marginal propensity to consume will likely weaken.

Over time, rising EMIs may crowd out savings and limit future spending capacity.

- Banking and NBFC Sector

Banks and NBFCs have been central to India’s retail credit boom. Both have shifted focus from corporate to consumer lending, leveraging digital distribution and risk models. This has fueled strong credit growth, NIM expansion, and earnings momentum.

Yet, the surge in unsecured retail loans personal loans, credit cards, and small-ticket financing — introduces credit quality risks. As leverage builds and repayment capacity stretches, delinquencies may rise, especially among lower-income borrowers. The RBI has already flagged rising risks in personal loans and tightened risk weights on such exposures.

NBFCs, with higher reliance on market funding, face liquidity risks and spread pressures in a stress scenario. A slowdown in repayments or tighter financial conditions could squeeze margins. The sector may pivot toward secured assets and co-lending partnerships with banks to sustain growth while managing risk.

In aggregate, while the retail credit cycle has supported financial earnings, its sustainability hinges on income growth, credit discipline, and macro stability. Any deterioration could weigh on sector valuations and the growth of the lending book and net interest income.

- Financial Markets

Equity markets have thus far rewarded the consumption and lending upcycle, boosting valuations in banks, NBFCs, autos, FMCG, and discretionary sectors.

But rising leverage introduces systemic fragility. If household balance sheets weaken, credit growth could stall, and asset quality concerns could pressure financial stocks. If credit quality deteriorates, a negative wealth effect could emerge, softening consumption and slowing GDP momentum.

Bond markets may also reprice risk, widening spreads for lenders exposed to unsecured credit.

A more cautious stance is warranted as India may transition from a credit-driven consumption boom to a phase where repayment capacity and financial prudence become key drivers of market sentiment.

Conclusion

India’s surging household debt reflects both financial deepening and emerging vulnerability. In the short term, it has powered growth and profits; in the long term, it could restrain consumption, strain lenders, and heighten macro risks.

The way forward requires a calibrated credit expansion, aligned with income growth and directed toward productive, asset-backed borrowing. For policymakers, lenders, and investors, the imperative is clear: shift the emphasis from the quantity of credit to the quality of credit.

True sustainable growth depends not merely on higher borrowing, but on responsible leverage that safeguards both household balance sheets and the financial system’s resilience.

At India’s present level of per capita income and economic development, no other major economy has witnessed such a rapid surge in credit expansion and consumption growth. This unprecedented trend, if left unchecked, risks becoming an “albatross around the neck” of the Indian economy over the next 4–5 years.

Comments are closed.