China’s Ghost Growth: Cement, Debt & the Illusion of Productivity

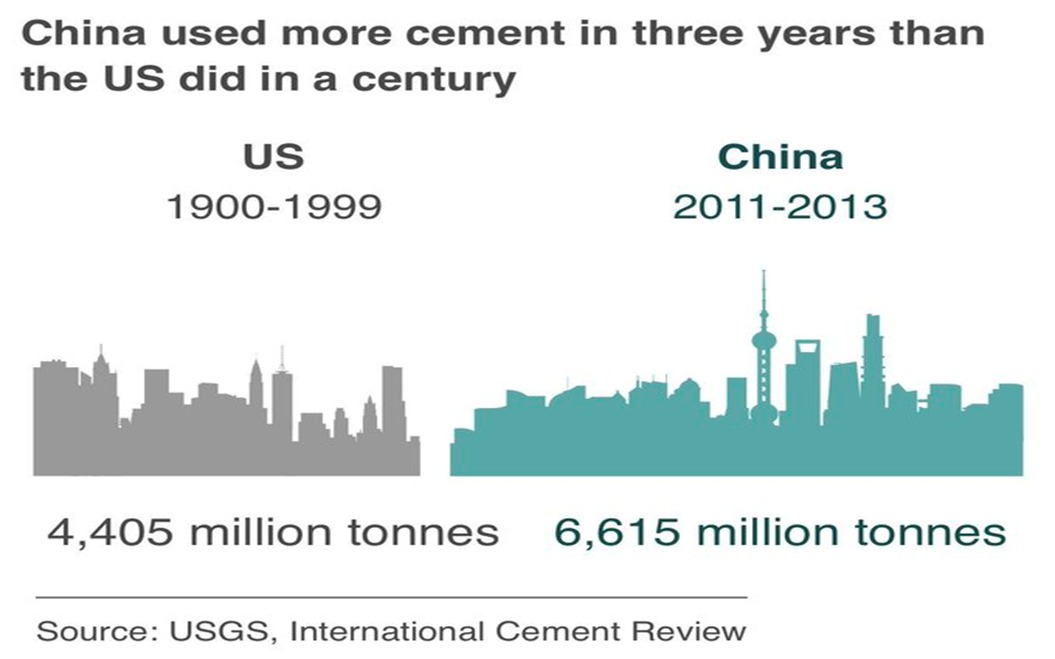

Between 2011 and 2013, China consumed 6.6 billion tonnes of cement, more than the US did in the entire 20th century. This extraordinary figure highlights China’s infrastructure-heavy development model, driven by real estate expansion, industrial overcapacity, and an evolving skyline.

However, beneath the surface lies an economy increasingly dependent on credit and investment-driven growth, with tens of millions of unsold apartments and thousands of inefficient state-backed enterprises now acting as economic dead weight.

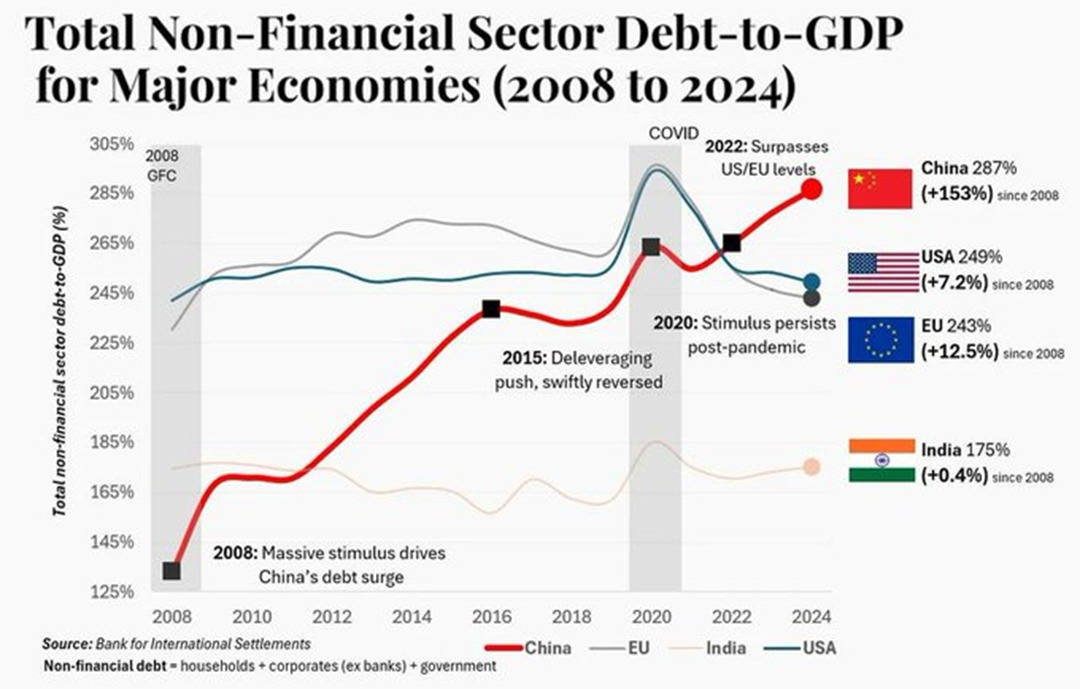

This second chart, showing China’s non-financial sector debt-to-GDP ratio, provides the other side of the equation. Since the Global Financial Crisis, China’s debt-to-GDP has ballooned from 125% to 287%a staggering +153% increase. Most of this debt has gone into funding real estate, local government financing vehicles (LGFVs), and infrastructure a large portion of which is now generating diminishing or zero economic returns.

This combination of:

- Unprecedented construction

- Soaring leverage

- And massively underutilized assets

This paints a picture of debt-fueled GDP increasingly divorced from genuine productivity growth.

Our View

We believe China is facing a muted and prolonged structural slowdown, shaped not just by the legacy of overbuilding and over borrowing, but increasingly by external and internal constraints on its next potential growth engines.

While the global AI boom has triggered massive investments in data centers and digital infrastructure, China’s participation remains limited. Export restrictions on advanced chips, tightening Western capital flows, and growing domestic regulatory uncertainty have significantly curbed its access to cutting-edge technology and global innovation capital.

Even as China accelerates AI-linked investment, the scale of capital flowing into AI remains relatively small compared to the country’s massive exposure to real estate, infrastructure, and construction. Even under optimistic scenarios, AI growth is unlikely to offset the economic drag caused by the structural downturn in these traditional sectors.

At the same time, the pressure is building within the banking system. With growing non-performing assets linked to struggling developers, overleveraged LGFVs, and weak industrial borrowers, China’s banks are under rising stress. If unaddressed, this could evolve into a broader banking or financial crisis, adding further to the country’s economic malaise.

In short, the old engines of growth are stalling, and the new ones are not yet strong enough to carry the load. Without deep reform and a strategic reset, China’s growth may remain subdued for an extended periodweighed down by structural imbalances and financial fragility.

Comments are closed.