The Illusion of Affordability: Housing Wealth’s Generational Shift

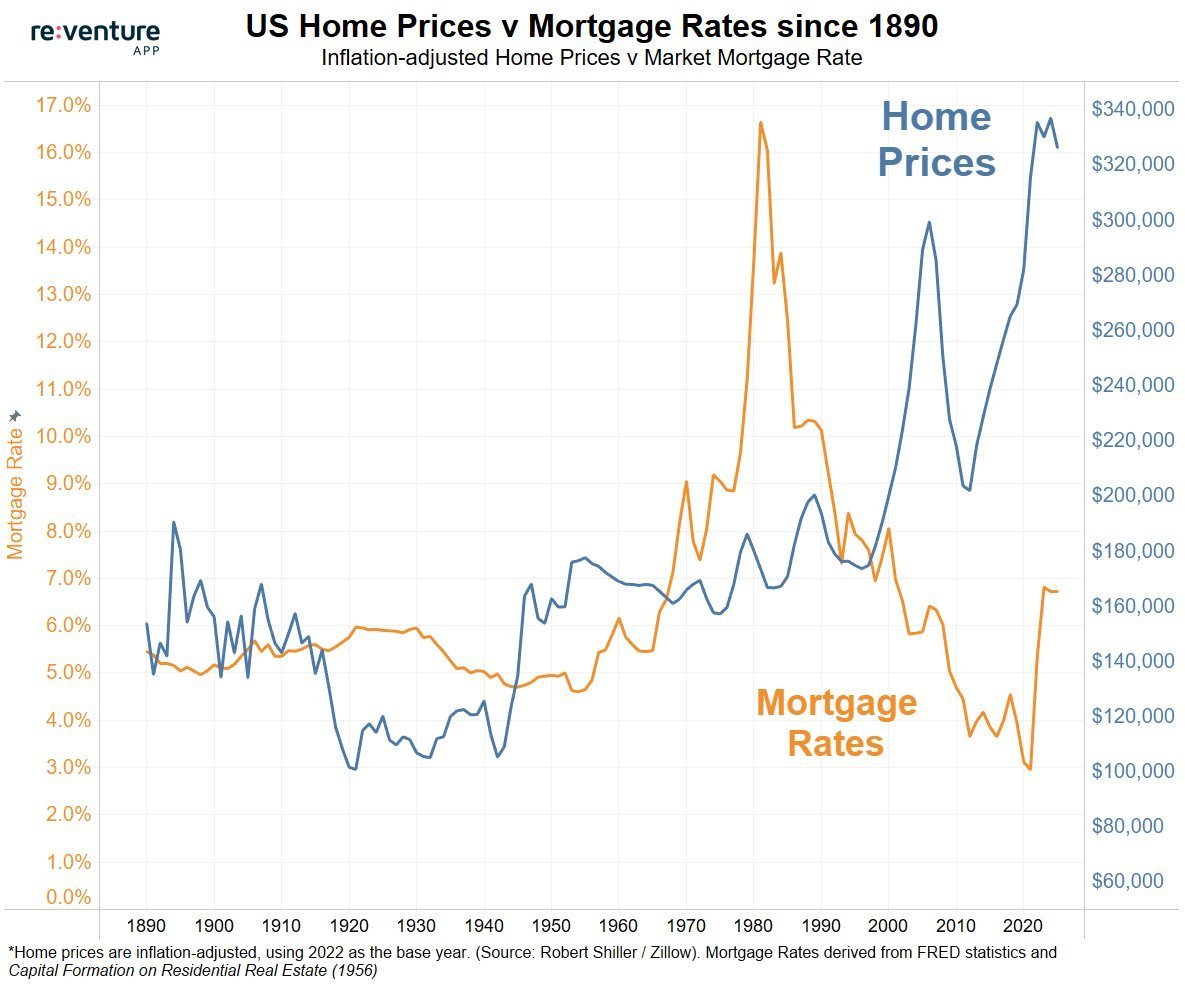

This first chart shows the dramatic moves in inflation-adjusted home prices and mortgage rates over the last 135 years. For most of the 20th century, inflation-adjusted home prices were relatively stable, moving sideways even as rates fluctuated. But after 2000, the story changed: falling mortgage rates created an affordability illusion, allowing prices to surge far beyond historical norms. The 2020 pandemic-era lows in interest rates ignited another leg higher, but the sharp rise in borrowing costs since 2022 has now left the market with record-high home prices and collapsing affordability.

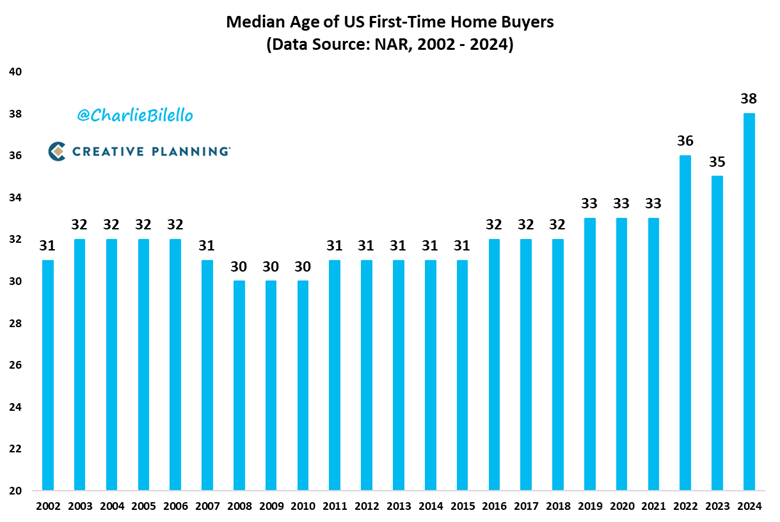

Now, this second chart highlights the consequences of that imbalance. The median age of US first-time home buyers has risen from around 30 in the early 2000s to 38 today the highest on record. A mix of rising student debt, delayed household formation, and deteriorating affordability has pushed younger generations out of the housing market. Unlike prior decades, where home ownership was a foundation of middle-class wealth building, today’s environment delays or even denies that pathway, concentrating housing wealth among older, asset-rich households.

Conclusion

The US housing market has shifted from a cyclical story of credit booms and busts to a structural divide rooted in affordability and demographics. Chart 1 shows how sharp disconnect between home prices and mortgage rates has created a market where home prices have broken away from the affordability dynamics implied by mortgage rates, while Chart 2 illustrates the real-world outcome: younger Americans are entering homeownership later than ever, if at all.

This shift carries lasting implications. Wealth accumulation through housing —once a near-universal middle-class steppingstone is increasingly limited to older generations who purchased earlier at lower costs. Younger households face rising barriers, which not only widens the generational wealth gap but also dampens the traditional economic flywheel of housing-driven consumption and investment.

In effect, the US has avoided the leverage-fueled fragility of 2008 but at the cost of entrenching social and generational fragility. In other words, while the financial system is more stable than in 2008, the social foundations of housing access have become weaker. Housing wealth is now more concentrated, mobility into ownership more restricted, and the economy more dependent on financial markets and corporate activity than broad-based household participation.Unless affordability improves, this generational divide could become a defining feature of the US economy stable on the surface, but increasingly unequal and disturbed at its core.

Comments are closed.