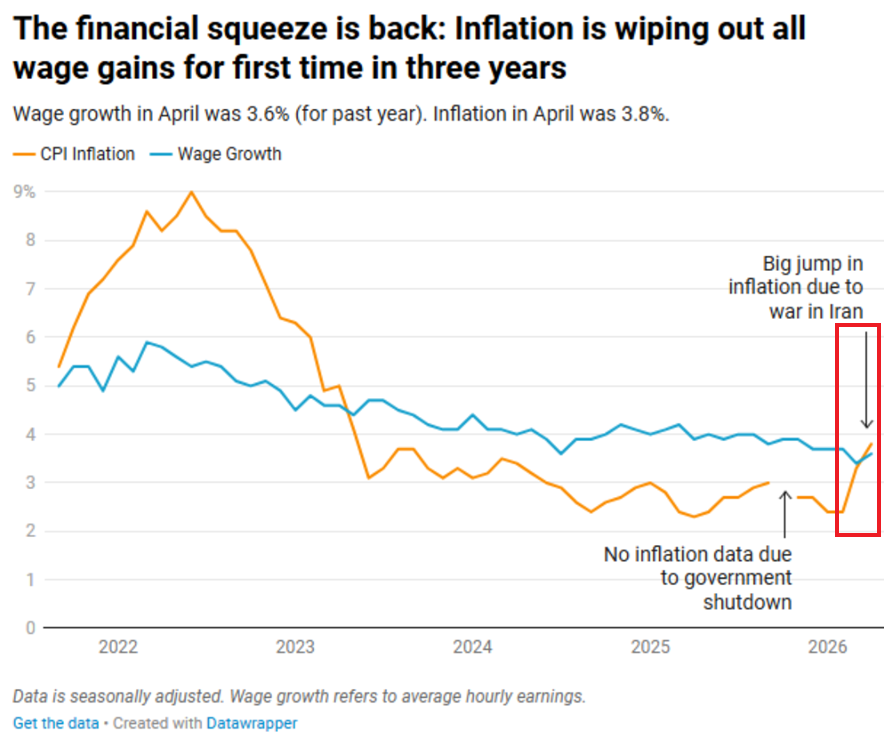

This chart shows that inflation is once again rising faster than wage growth, creating renewed pressure on consumers and weakening real purchasing power. The recent rise in inflation has been driven largely by higher oil prices and geopolitical tensions linked to the Iran conflict, making essentials like fuel, food, and transportation more expensive. At the same time, wage growth is slowing, which could reduce consumer spending and weaken economic momentum. In the current market environment, this raise concerns that central banks may need to keep interest rates higher for longer, increasing the risk of slower growth, persistent inflation, and higher volatility across the global economy.

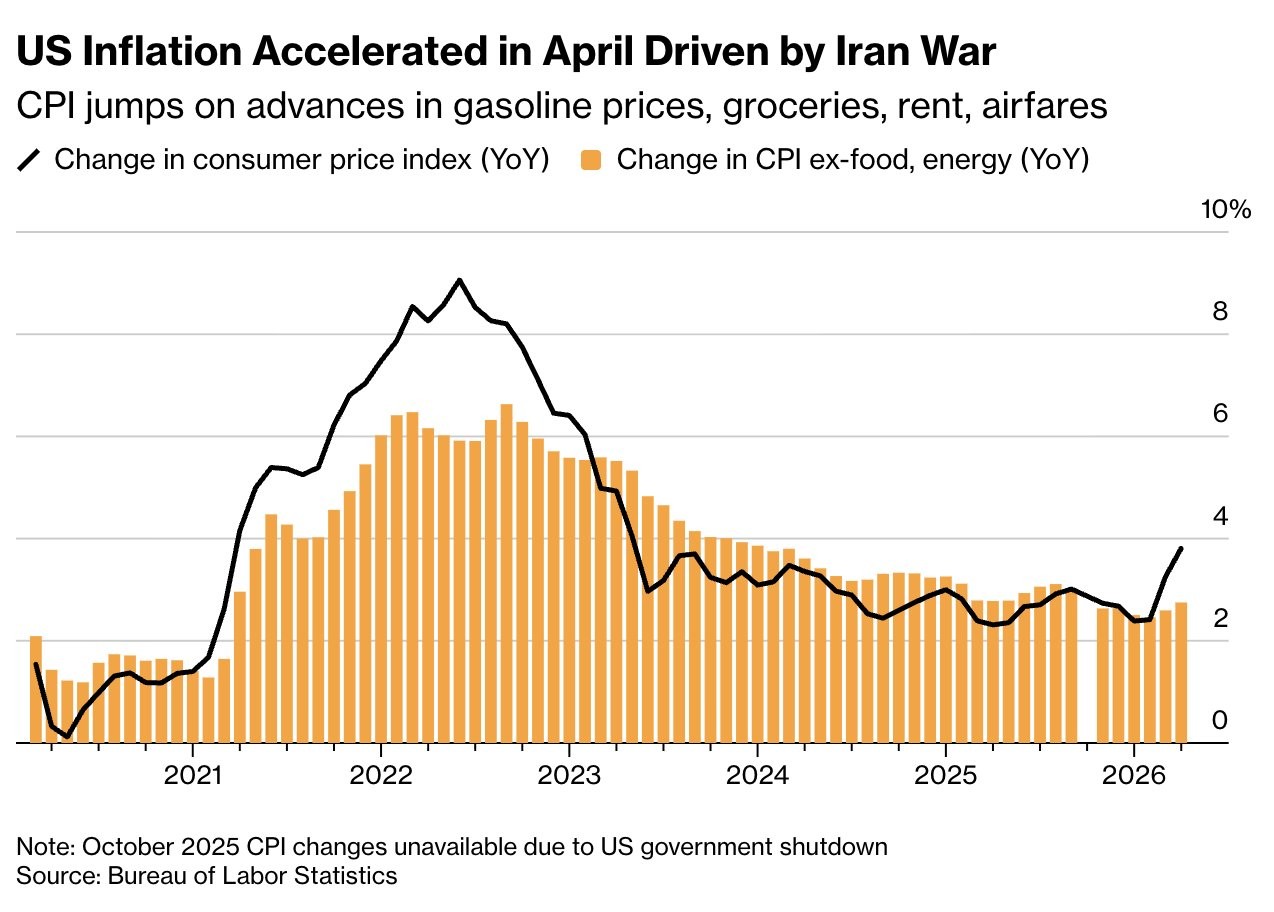

This chart shows that US inflation is rising again, with higher gasoline prices from the Iran conflict pushing up broader consumer costs such as groceries, rent, and travel. The increase in headline CPI suggests that energy-driven inflation is spreading across the economy rather than staying limited to fuel prices. At the same time, core inflation remains relatively sticky, indicating that price pressures are still embedded in everyday spending and services.

In the current market environment, this raise concerns that inflation could stay elevated for longer than expected. As businesses continue passing higher energy and transportation costs onto consumers, the Federal Reserve may be forced to keep interest rates higher for longer, increasing risks for economic growth, consumer spending, and market stability.

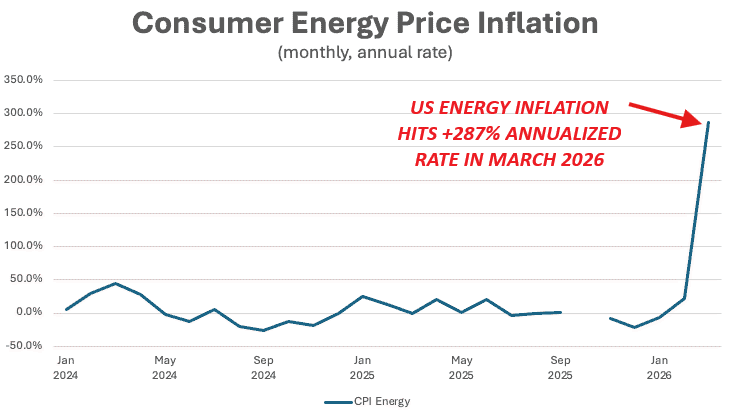

This chart shows that US energy inflation is accelerating sharply rather than rising gradually, with annualized energy prices surging nearly 287% by March 2026. The parabolic move visible in March reflects severe stress in energy markets caused by tightening oil supplies, falling inventories, and geopolitical disruptions affecting global crude flows. The temporary gap in the data during the shutdown period makes the rebound appear even more dramatic once reporting resumed, clearly showing how rapidly energy prices spiked in a short time. Such sudden moves usually signal growing fears that supply shortages may persist for a longer period rather than remain temporary.

The concern is that rising energy costs quickly spread across the broader economy through transportation, utilities, logistics, and household expenses, increasing overall inflation pressures. In the current macro environment, this sharp rebound in energy inflation raises risks of weaker consumer purchasing power, slower economic growth, and higher financial market volatility if elevated energy prices continue for an extended period.

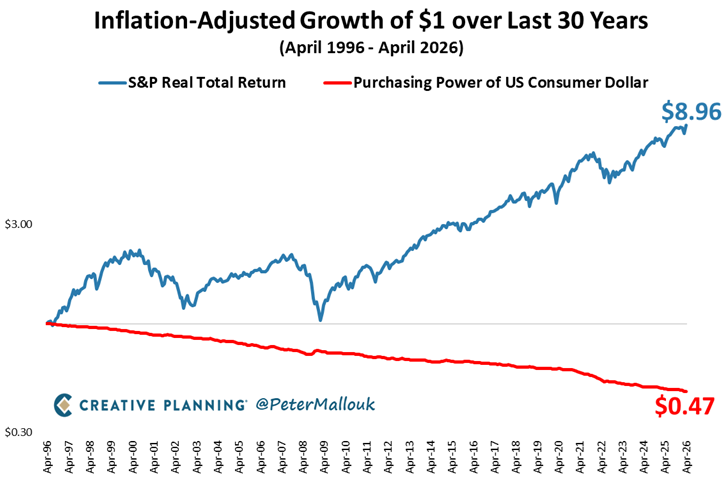

This chart highlights the long-term impact inflation has had on the purchasing power of the US dollar compared with the growth of financial assets. Over the last 30 years, $1 invested in the S&P 500 grew to nearly $8.96 on an inflation-adjusted basis. The purchasing power of the average consumer dollar steadily declined to around $0.47. In simple terms, the dollar today buys less than half of what it could in the mid-1990s, showing how persistent inflation gradually erodes the real value of money over time. In terms of US equities, the real purchasing value of the dollar has gone down by around 95%.

In the current macro environment, this concern is becoming even more significant as inflation risks rise again due to higher energy prices, geopolitical tensions, supply-chain disruptions, and elevated global debt levels. The recent rebound in commodity and energy inflation is increasing fears that purchasing power may weaken further in the coming years. The chart also explains why investors increasingly shift toward equities, commodities, gold, and other real assets during inflationary periods, as they seek protection against the long-term erosion of currency value and the declining real strength of cash holdings.

Conclusion

Overall, the charts collectively point toward a global economy becoming increasingly vulnerable to inflationary shocks driven by energy, geopolitics, and structural supply constraints. Rapidly rising oil and energy costs, weakening purchasing power, elevated debt levels, and growing dependence on a narrow set of growth drivers are creating a fragile macro environment where inflation risks remain persistent even as economic momentum slows. The broader concern is that if these pressures continue simultaneously, the world economy could face a prolonged period of slower growth, higher volatility, and reduced financial stability across both consumers and markets.