Echoes of 2000, Lessons for 2025: The Rise of Tech and Fall of Safety

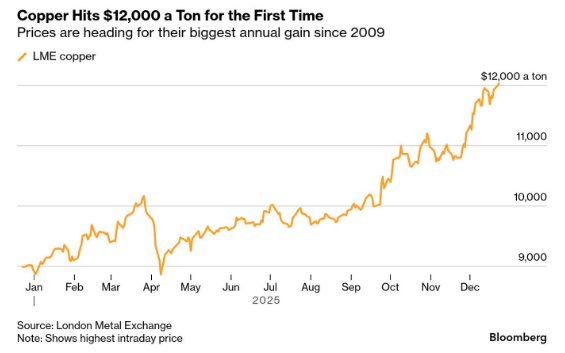

Copper’s breakout to record highs is increasingly reflecting a structural repricing rather than a cyclical spike, with the metal now showing clear potential to move further higher as its role in the global economy expands. Demand is no longer limited to traditional construction and manufacturing; it is being structurally lifted by electrification, EV penetration, renewable energy grids, data centers, AI-driven power infrastructure, and large-scale transmission upgrades—all of which are copper-intensive and non-substitutable. At the same time, supply remains inelastic due to declining ore grades, underinvestment in new mines, long permitting cycles, and geopolitical concentration of production, creating a persistent demand–supply imbalance. This dynamic mirrors what has already played out in silver during 2025, where the metal outperformed most asset classes as industrial demand converged with investment flows, forcing a valuation reset. Copper now appears to be entering a similar phase, where higher usage intensity and strategic importance are driving sustained price strength rather than speculative excess. In the current macro environment, copper is evolving into a critical growth and scarcity asset, suggesting that elevated prices may not signal a peak but rather a new equilibrium shaped by long-term structural demand.

Beyond the immediate price action, the alignment between forward supply projections and recent market behavior suggests that copper is transitioning into a scarcity-led pricing regime. Inventories across exchanges and supply chains are already thin, reducing the buffer that typically absorbs demand shocks. At the same time, new mine approvals, capital expenditure cycles, and geopolitical risks around key producing regions imply that supply responses are likely to be delayed and uneven. This creates an environment where even incremental demand surprises can have an outsized impact on prices. From a macro perspective, copper is increasingly functioning as a strategic input rather than a traditional industrial commodity, with its availability becoming a constraint on infrastructure execution itself. Taken together, the charts point to a market where tight balances translate directly into higher clearing prices, reinforcing copper’s role as a critical bottleneck metal in the next phase of global growth rather than a late-cycle trade.

Conclusion

Taken together, the price breakout and the forward supply outlook indicate that copper is moving into a phase where equilibrium is no longer set by short-term cycles but by long-term resource constraints. The market is showing that future availability is becoming increasingly uncertain, forcing prices to adjust in advance rather than reactively. These dynamic shifts copper from being a follower of global growth to a driver of cost structures across infrastructure and manufacturing. As deficits deepen over the coming years, price volatility is likely to remain skewed to the upside, not because of speculative excess, but because the system lacks sufficient slack to absorb sustained demand. In this context, copper prices appear less vulnerable to quick mean reversion and more anchored to a structurally higher range, reflecting a durable re-rating of the metal’s strategic importance.

Macro Implications

At the macro level, this copper dynamic has important second-order effects that extend beyond the metal itself. Persistently elevated copper prices increase the capital intensity of power networks, renewable projects, housing, and industrial expansion, potentially slowing project execution or raising financing needs. This introduces a new channel of cost pressure into the global economy, particularly for emerging markets and infrastructure-heavy growth models. For policymakers, it complicates the inflation outlook by shifting pressure from energy to materials, reducing the effectiveness of traditional disinflation drivers. For markets, it reinforces a preference for real assets and upstream resource exposure, while increasing earnings risk for downstream manufacturers unable to pass through higher input costs. Overall, copper’s tightening balance points to a macro environment where physical constraints, rather than demand stimulus, increasingly shape growth, inflation, and investment cycles.

Comments are closed.