Record Tech Concentration, Fading Profits: A Market onThin Ice

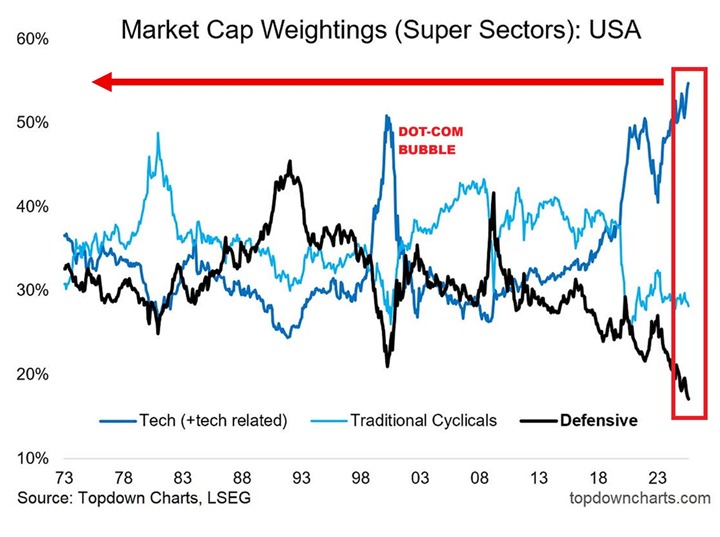

This first chart shows that US technology and tech-related stocks now make up 55% of total market capthe highest share in history, even above the Dot-Com Bubble peak. Defensive sectors, by contrast, have been pushed to just 18%. This means the entire market has become a one-sector bet: if mega-cap tech stumbles, the index stumbles with it.

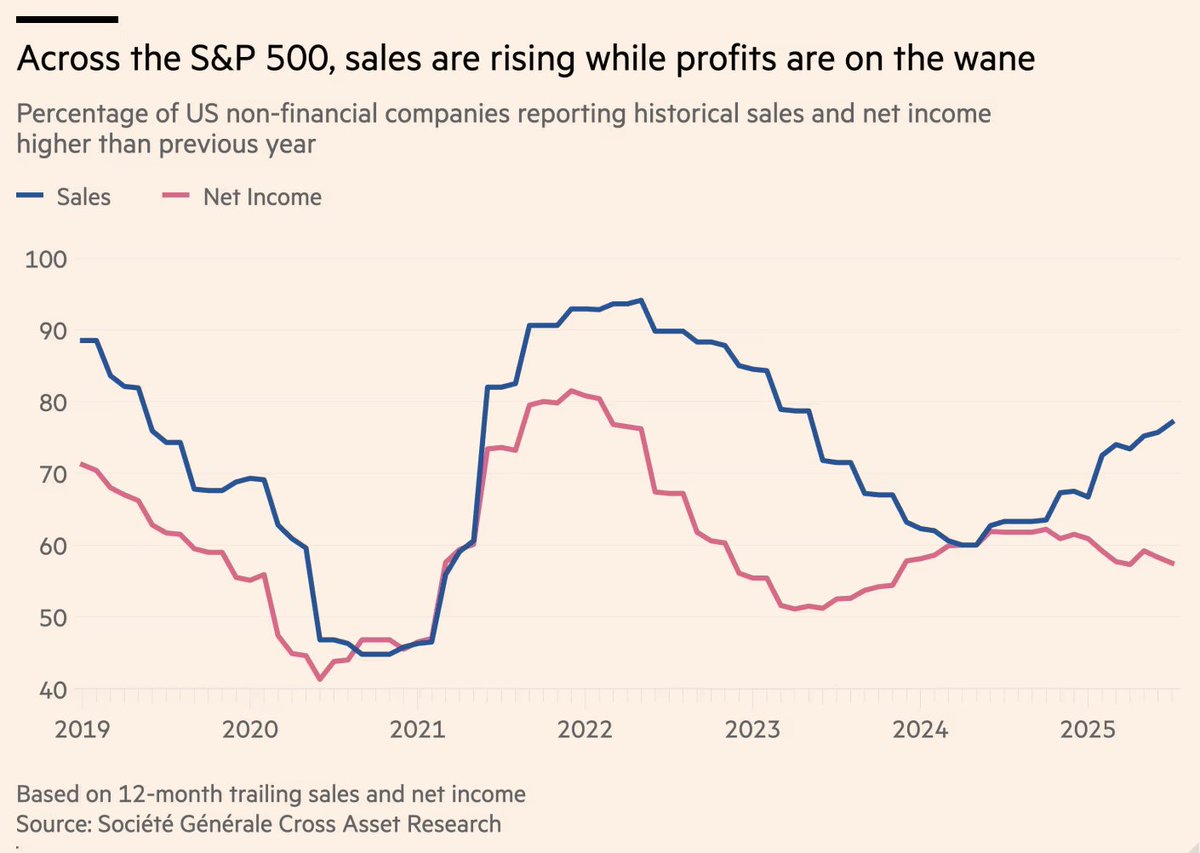

This second chart adds another layer of concern. While sales across S&P 500 companies are rising, the share of firms reporting higher net income has been trending steadily lower since 2022. This reveals that revenue growth is not translating into profitability, margins are under pressure from rising costs and heavy AI-related capex. In effect, investors are rewarding top-line growth at the very moment bottom-line strength is fading.

This combination is troubling. Valuations are at record highs for tech, the very sector now carrying the index and overall corporate profitability is deteriorating. The setup looks eerily similar to late-cycle markets of the past: narrow leadership, crowded trades, and earnings momentum that no longer matches the hype.

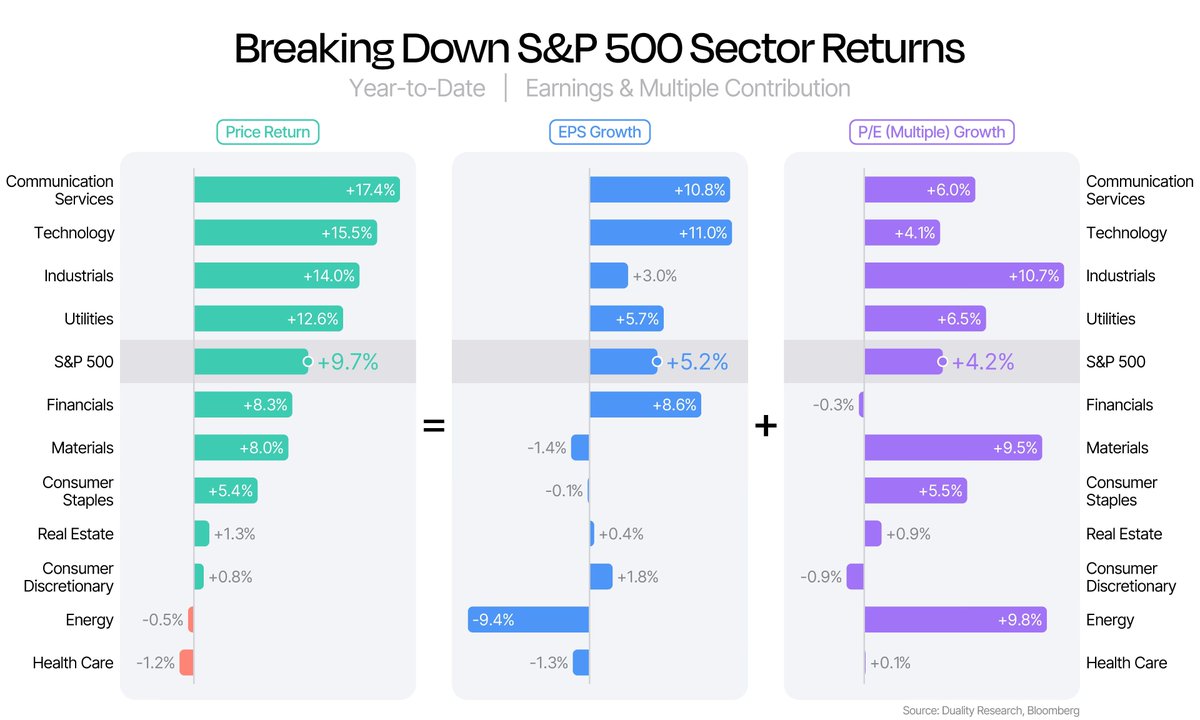

Now this third chart makes it clear: if we break down S&P 500 sector returns, the fragility stands out. Nearly 45% of the Year-to-date gains have come from P/E multiple expansion. Technology, industrials, and even materials show that most of the rise in prices has been driven by higher valuations rather than higher profits. Much of the much talked about EPS growth has been fueled by the AI frenzy and outsized bets on data centers and cloud, but that is clearly unsustainable over the long term.

This is a dangerously potent mix: profit growth is expected to slow down, margins are under pressure, and yet valuations are stretching higher. Normally, such conditions would lead to P/E contraction, not expansion. The fact that multiples are inflating signals that the market has become extremely vulnerable to any shift in sentiment or earnings disappointment.

Conclusion

What we’re witnessing in U.S. equities—and particularly in Tech—is not broad-based strength in the economy or corporate sector, but a market built on overly optimistic and fragile foundations. Extreme tech concentration has left investors with fewer shock absorbers, while adeteriorating earnings profile is being overlooked. Momentum has already started to roll over: instead of pushing prices higher, it is turning into a drag. With sentiment cracking and fundamentals weakening,downside risks are no longer theoretical—the correction phase has already begun.

Comments are closed.