Echoes of 2000, Lessons for 2025: The Rise of Tech and Fall of Safety

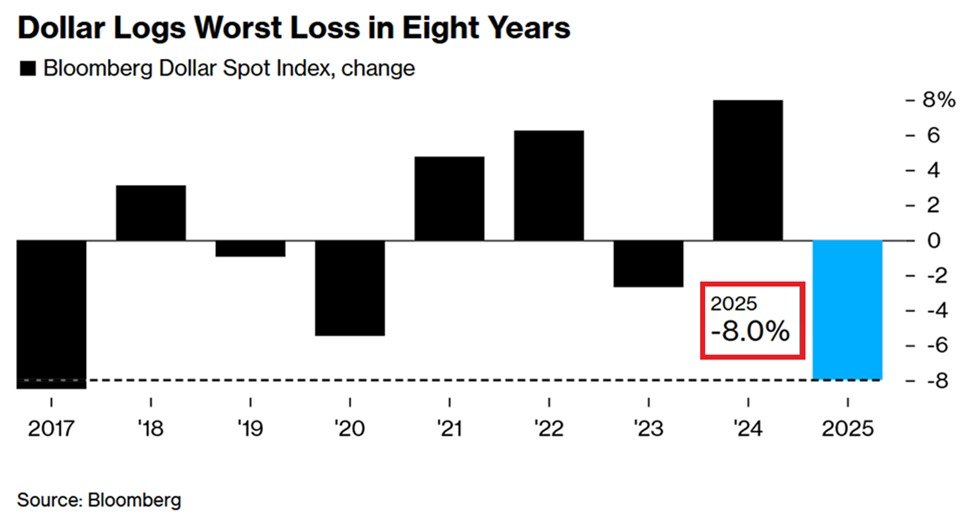

The chart shows the Bloomberg Dollar Spot Index falling ~8% in 2025, its worst annual decline in eight years, marking a clear shift from the strong dollar cycle of 2021–22. This weakness is mainly driven by repricing of US interest rates, as easing inflation and slower growth reduced the dollar’s yield advantage after a prolonged period of tight monetary policy. Heavy bearish positioning further amplified the move, turning the decline into a cyclical overshoot rather than a loss of confidence in the currency.

Trade and tariff dynamics and massive twin deficits have added pressure on the Dollar in CY 2025 . Rising tariffs and fragmented trade flows increase domestic cost pressures in the US but also put economic pressure on businesses, limiting how restrictive the Federal Reserve can remain. This compresses real yields and encourages countries to diversify settlement mechanisms, marginally reducing transactional demand for the dollar without displacing its global role.

A softer dollar has directly supported precious metals, which benefit from falling real yields, geopolitical uncertainty, and central bank buying as a hedge against policy and sanctions risk. At the same time, commodities have gained tailwinds both from dollar weakness and from supply-side constraints tied to energy security, infrastructure spending, and the energy transition.

Importantly, higher commodity prices and persistent inflation risks tend to stabilize US real yields over time, drawing defensive capital back toward the dollar. This creates conditions for a short-term dollar bounce, even as longer-term reserve diversification and multipolar trade trends continue gradually in the background.

When this long-term Dollar Spot Index trend chart is read alongside the 2025 annual performance chart, a clear time-frame divergence emerges. The earlier chart captured the speed and magnitude of the 2025 selloff, while this chart explains the structural setup behind it.

This second chart shows the dollar still sitting near a two-decade rising trendline, built from post-2008 crisis lows. The recent weakness has pushed the index toward this long-term support, not decisively through it. Historically, when the dollar tests such multi-year trendlines after sharp annual declines, it tends to rebound first, driven by technical mean reversion, defensive flows, and repositioning by long-term investors.

This sets up a 2026 rebound phase, as the trendline acts as a magnet for stabilization and short covering. A recovery does not require new bullish fundamentals — only a pause in negative surprises and normalization of expectations after an extreme down year. This rebound would likely be corrective rather than trend changing.

However, the same chart also signals that each successive dollar rally has produced lower momentum over the past decade, indicating long-term exhaustion. Once a rebound plays out, the repeated tests of this trendline increase the probability of an eventual breakdown. That would mark a structural transition from a rising to a declining long-term dollar cycle, reflecting a gradual shift toward a multipolar currency and asset system.

Conclusion

Viewed together, the two charts suggest the dollar is transitioning from shock-driven weakness to a phase of tactical recovery, rather than entering an immediate collapse. The sharp 2025 decline reflects an accelerated adjustment that has brought the dollar back to levels where long-term participants typically re-engage. This creates room for a cyclical rebound in 2026, driven by stabilization in positioning, policy expectations, and risk sentiment. We estimate that Dollar Index could easily climb back to 105 levels in CY 2026.

Beyond that rebound, the repeated erosion of trend support over multiple cycles points to a slow structural rollover, not a sudden break. Future dollar strength is likely to be increasingly met with diversification flows. In effect, the charts together frame a regime shift: near-term resilience followed by a prolonged, grinding downward trajectory, consistent with a more fragmented global monetary order rather than a single dominant reserve currency.

Macro Implications:

A near-term sharp dollar rebound would tighten global financial conditions temporarily, creating short-lived pressure on emerging market currencies, commodities, and risk assets as capital rotates back toward dollar liquidity. This phase may also cool inflation expectations marginally, allowing policymakers to regain some policy space.

Over the longer horizon, a sustained downward dollar trajectory would reshape global capital allocation. Trade invoicing and reserve strategies would increasingly favor non-USD assets, reinforcing demand for real assets, alternative settlement systems, and regional currency blocks. This shift would support structurally higher commodity floors, greater FX volatility, and a more persistent inflation premium globally. The result is a macro environment defined less by dollar dominance and more by cyclical dollar strength within a broader secular decline, altering how risk, hedging, and policy transmission function worldwide.

Comments are closed.