AI Euphoria Meets Reality: Capex Is Surging Faster Than Profits

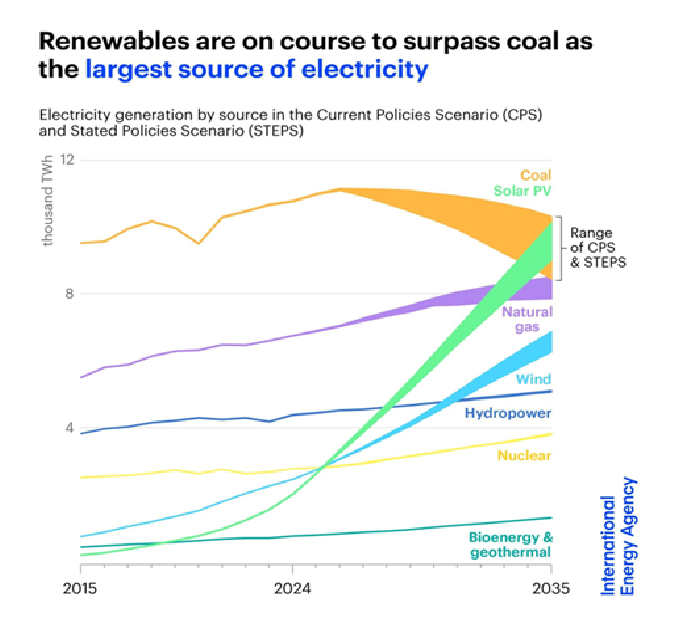

The chart shows a structural shift in global power generation, with solar and wind rapidly scaling and set to overtake coal as the dominant energy sources. Solar PV is the core growth drive, fueled by sharp cost declines, manufacturing scale, and fast efficiency gains, with unmatched scalability from rooftop systems to utility-scale projects. Wind complements solar by providing diversified and seasonal generation, while coal faces secular decline due to weak economic and policy pressure. Natural gas acts as a transition fuel, and nuclear and hydropower remain constrained by geography, timelines, and capital intensity.

This transition marks a reordering of the global energy hierarchy, with renewables moving from marginal supply to core baseload power. Solar’s dominance in new capacity makes it the marginal price setter, structurally lowering electricity prices and accelerating electrification. Lower energy costs and emissions position clean power as a key pillar of future growth, reshaping capital allocation, industrial competitiveness, inflation dynamics, and equity sector leadership across utilities, manufacturing, and infrastructure.

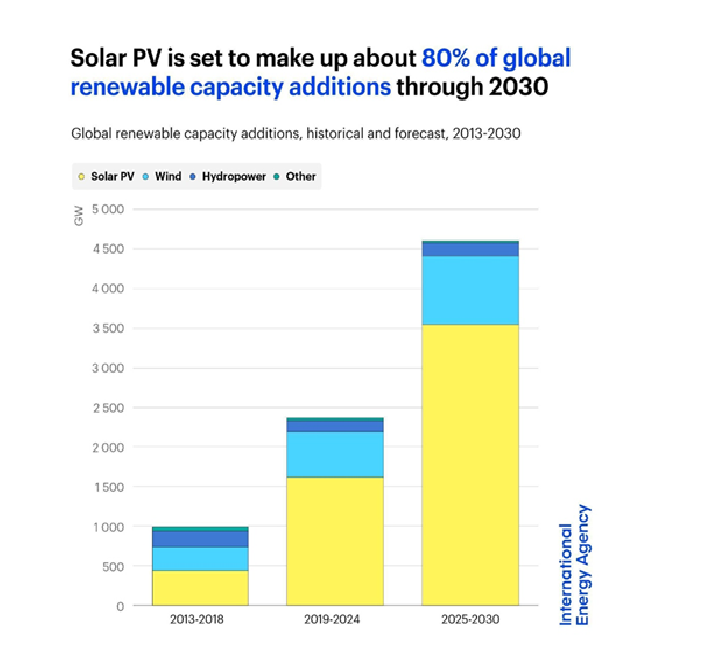

The chart highlights the growing dominance of solar PV in global renewable energy expansion, with solar expected to contribute nearly 80% of new renewable capacity additions through 2030. This reflects a sharp acceleration in solar deployment compared to wind, hydropower, and other renewables, which are growing at a more gradual pace.

Solar’s rapid rise is driven by its low cost, fast deployment cycle, and scalability, making it the most practical solution to meet surging electricity demand from AI data centers, EV adoption, and industrial electrification, alongside global decarbonization policies. As a result, capital is increasingly flowing into solar manufacturing, grid infrastructure, storage, and transmission, allowing solar to capture the largest share of the renewable energy market.

While wind, hydro, and nuclear remain important for system stability and diversification, they face structural constraints such as geography, high capital intensity, and regulatory delays. Consequently, solar is emerging as the primary marginal power source shaping future electricity prices, emissions trajectories, and energy security frameworks.

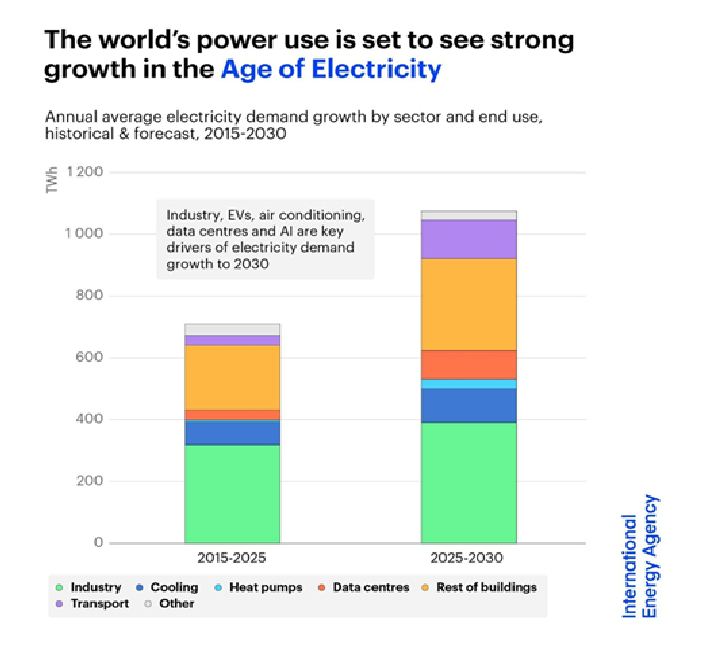

This chart confirms that the global economy is entering a structurally electricity-intensive growth phase, with demand accelerating sharply into 2025–2030. Industry, EVs, cooling, and especially data centers are emerging as the dominant marginal drivers of power consumption, signaling that digitalization and electrification are becoming core pillars of economic expansion rather than cyclical themes.

When read alongside the earlier charts showing Solar’s dominance in capacity additions and investment flows, it becomes clear that electricity demand growth is structurally aligned with renewable supply growth, particularly solar PV. The power system is being redesigned around scalable, low-cost renewable generation to meet this new demand profile.

Conclusion

Together, these charts illustrate a structural inflection point in the global energy and economic cycle. Electricity demand is entering a secular acceleration phase driven by AI data centers, EVs, industrial electrification, cooling needs, and digital infrastructure, marking a shift toward an electricity-centric growth model. At the same time, solar PV is emerging as the dominant marginal power source due to its cost advantage, scalability, and rapid deployment capability, capturing the bulk of new renewable capacity and investment flows.

This alignment between surging electricity demand and solar-led renewable supply triggering a multi-decade capital expenditure cycle across generation, grids, storage, transmission, and critical metals. The transition is not only reshaping the energy sector but also redefining macroeconomic dynamics, lower structural energy costs, improved energy security, new industrial supply chains, and shifting geopolitical leverage toward countries that control renewable technologies and manufacturing ecosystems.

Comments are closed.