AI Euphoria Meets Reality: Capex Is Surging Faster Than Profits

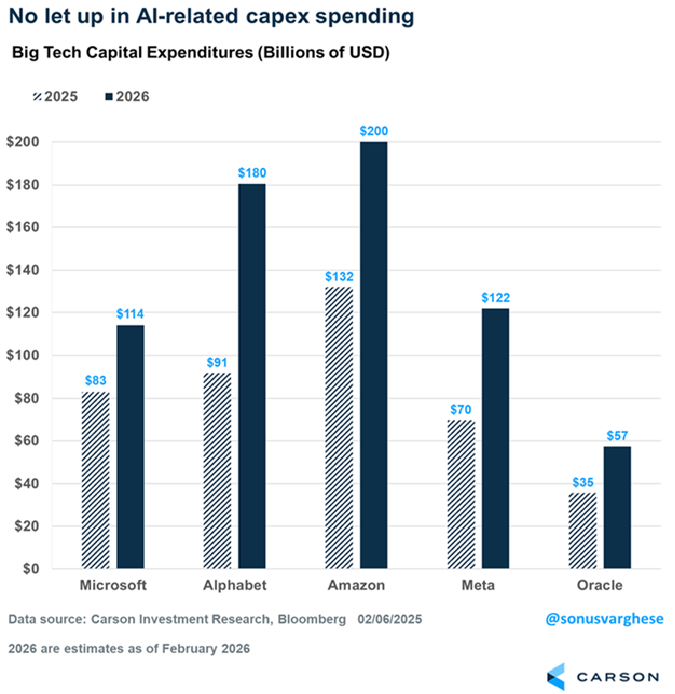

The chart shows that Big Tech companies are continuing to aggressively increase AI-related capital expenditure (Capex) in 2026 compared to 2025, signaling that the AI investment cycle is still accelerating rather than slowing down. Amazon and Alphabet are leading the spending surge, followed by Microsoft and Meta, while Oracle is also ramping up investment, though at a smaller scale. The sharp year-over-year increase across all companies indicates that the AI infrastructure buildout—data centers, chips, cloud capacity, and models—is entering a massive scale-up phase, reflecting strong corporate conviction in long-term AI monetization despite rising stakes. This sustained Capex expansion suggests a tech investment Supercycle getting even more prolonged, with potential pressures on profits and cash flows.

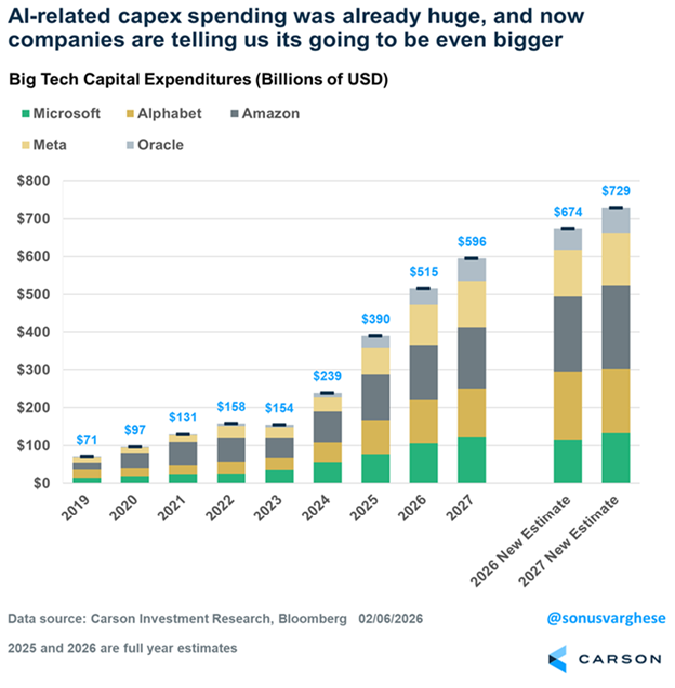

This chart shows that AI-related capital expenditure by Big Tech has been rising structurally since 2019 and is now projected to accelerate sharply into 2026–2027, indicating that the AI investment cycle is not a short-term trend but a multi-year infrastructure buildout. The stacked bars highlight that spending is broad-based across Microsoft, Alphabet, Amazon, Meta, and Oracle, meaning AI is becoming a core capital allocation priority across the entire tech ecosystem rather than a single-company race. The step-change after 2024 reflects the transition from experimental AI spending to full-scale industrial deployment, including massive data center expansion, custom chips, and cloud capacity. The upward revision in 2026 and 2027 estimates suggest companies themselves expect AI demand to grow faster than previously anticipated. If the incremental revenues take longer to come through, it will put enormous pressure on the entire Tech Eco-system in US and the rest of the world.

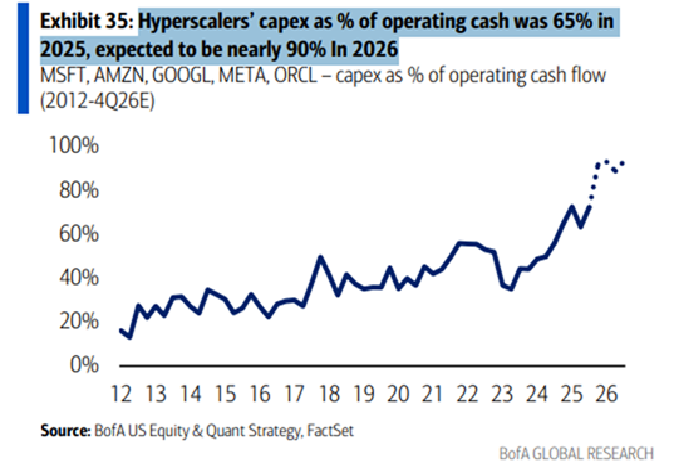

This chart shows that hyperscale’s’ capital expenditure as a share of operating cash flow is rising sharply, moving from around 65% in 2025 to nearly 90% projected in 2026. This means tech giants are expected to reinvest almost all their internally generated cash back into infrastructure, leaving very little buffer for dividends, buybacks, or balance sheet flexibility. The steep jump from 2025 to 2026 indicates an acceleration in spending intensity rather than a gradual investment cycle, signaling that companies are pushing capital deployment to historically extreme levels. Such high reinvestment ratios typically mark late-cycle phases of capital booms, where incremental returns on capital become uncertain and execution risks increase significantly.

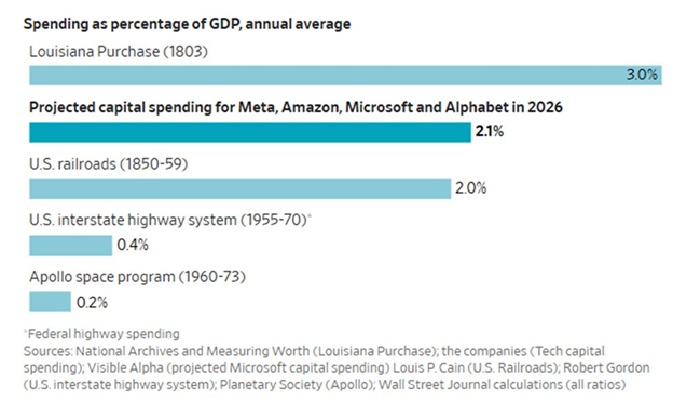

This chart puts the current AI spending cycle into historical context and shows that projected capital expenditure by a handful of Big Tech firms in 2026 will reach levels comparable to some of the largest nation-building projects in U.S. history as a share of GDP. When combined with the earlier charts showing the exponential rise in AI Capex and the dominance of mega-cap tech in equity markets, it reveals that the technology sector is entering an unprecedented capital intensity phase where private companies are deploying resources at a scale once reserved for governments.

The aggressiveness of 2026 spending implies a significant front-loading of cash flows into infrastructure, which will structurally compress free cash flow and margins in the near term, despite strong revenue growth narratives. This creates a macro setup where tech valuations remain highly sensitive to interest rates and growth expectations, as elevated Capex reduces shareholder returns and increases execution risk. In equity markets already heavily concentrated in a few tech giants, this investment surge increases downside asymmetry: if AI monetization lags expectations, the profit cycle could underperform the capital cycle, leading to valuation de-rating and broader index pressure.

Conclusion

The combined evidence from these charts suggests that the current AI-driven tech cycle is becoming increasingly overstretched, with equity valuations running ahead of the underlying economic returns while capital commitments continue to escalate. Big Tech is committing record levels of investment, creating a narrowing margin for errors. As capital intensity rises, the burden on these companies to convert AI infrastructure into sustainable revenue and profit will intensify, and any delay in monetization could expose a gap between expectations and reality. This dynamic increases the risk of valuation compression and relative underperformance in tech, especially if financial returns fail to keep pace with the scale of capital deployed. A significant delay in the coming through of revenue could result in a rapid slowing down in incremental investment commitment by Tech companies, which could cause a US recession as has happened after every significant Capex push in each of the previous Industrial/ Technological revolutions over the last 300 years.

Comments are closed.