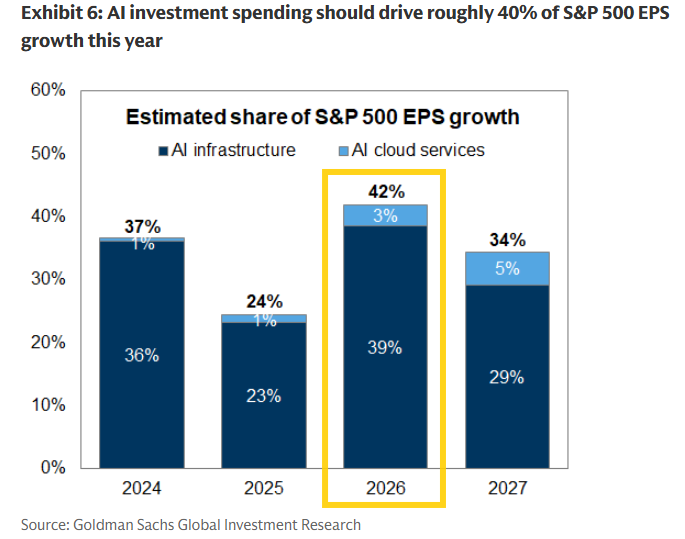

This chart highlights how strongly the current S&P 500 earnings growth is being driven by artificial intelligence spending. In 2026, nearly 42% of total EPS growth is expected to come from AI-related investment, with the largest contribution coming from AI infrastructure such as semiconductors, datacenters, networking systems, and computing hardware, while AI cloud services contribute a smaller share. This shows that corporate profit growth is becoming increasingly dependent on continued AI capital expenditure rather than broad-based economic expansion across multiple sectors.

In the current market environment, this helps explain why AI-linked technology companies continue to dominate market performance despite slower global growth, high interest rates, and ongoing geopolitical uncertainty. Investors are viewing AI as the primary long-term growth driver, leading to aggressive spending by major technology companies and cloud providers on chips, cloud capacity, and AI infrastructure. At the same time, the chart also points to rising concentration risk, where a large portion of market earnings and valuations are tied to one dominant theme.

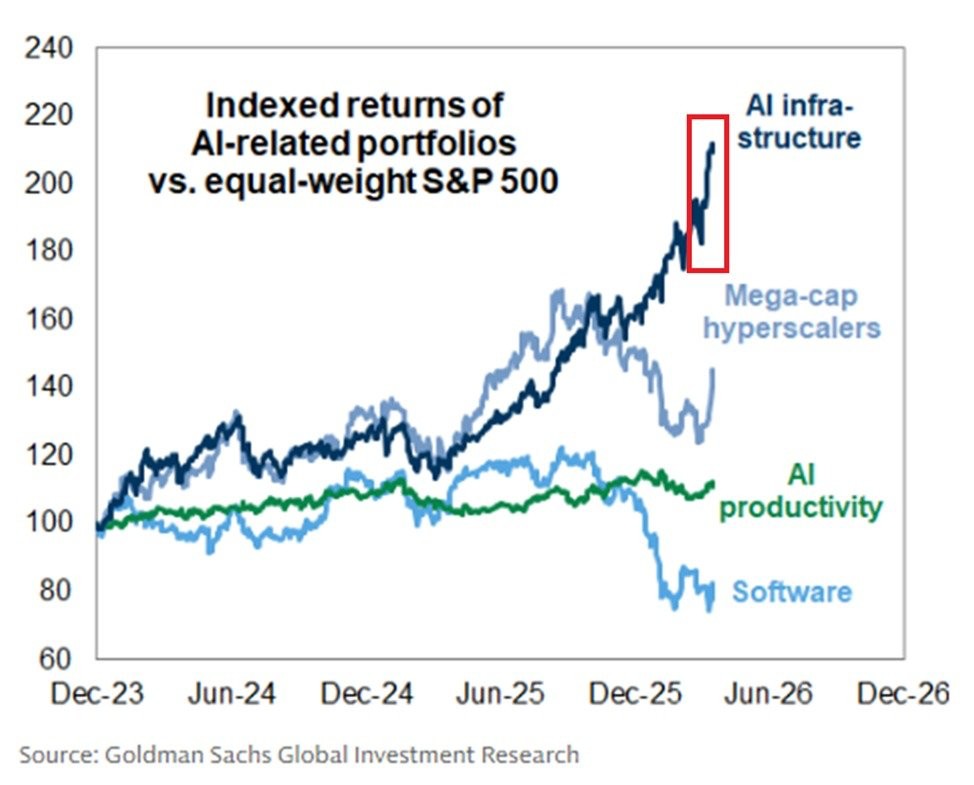

When viewed together with the previous chart, this data shows that the current AI-driven rally is being led mainly by infrastructure-related companies such as semiconductors, datacenters, networking, and hardware providers. Investors continue allocating aggressive capital toward these segments as major technology companies expand AI systems, cloud capacity, and computing power. This has made AI infrastructure one of the strongest drivers of both market performance and earnings growth in the S&P 500.

At the same time, the growing concentration around AI spending also creates a structural risk for markets. A large portion of market momentum and economic optimism is now dependent on continued AI investment. If spending slows in the near to medium term, sectors heavily exposed to AI infrastructure could face significant pressure, potentially creating broader volatility across equities and weakening overall growth expectations.

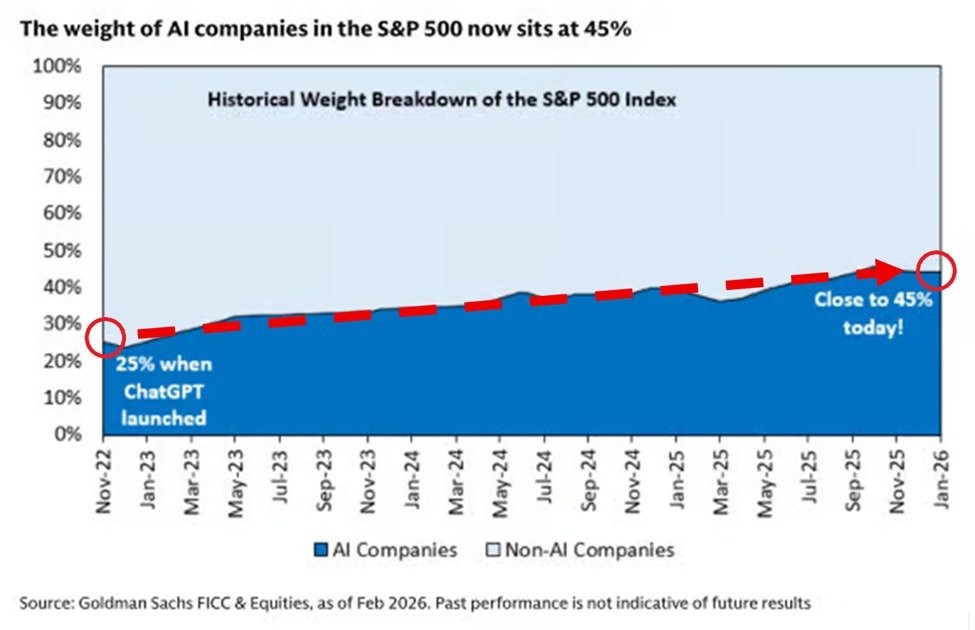

Building on the previous chart, this data highlights how concentrated the current market rally has become around AI-related companies. Since the launch of ChatGPT, the weight of AI-linked companies in the S&P 500 has risen sharply from nearly 25% to around 45%, showing that a large share of index performance is now dependent on a relatively small group of AI-driven firms. This aligns with the earlier chart where AI infrastructure companies were significantly outperforming the broader market, indicating that capital flows are increasingly concentrated in companies benefiting directly from the AI investment cycle.

The chart also suggests that market sensitivity to AI spending has increased substantially. As major technology companies continue allocating massive capital toward chips, datacenters, and cloud infrastructure, investor optimism remains strong. However, such high concentration also creates a structural risk for the broader market. If AI-related spending slows in the near to medium term, or if returns on these investments fail to meet expectations, the impact may extend beyond technology stocks and create broader pressure across the S&P 500 due to the index’s heavy exposure to AI-linked companies.

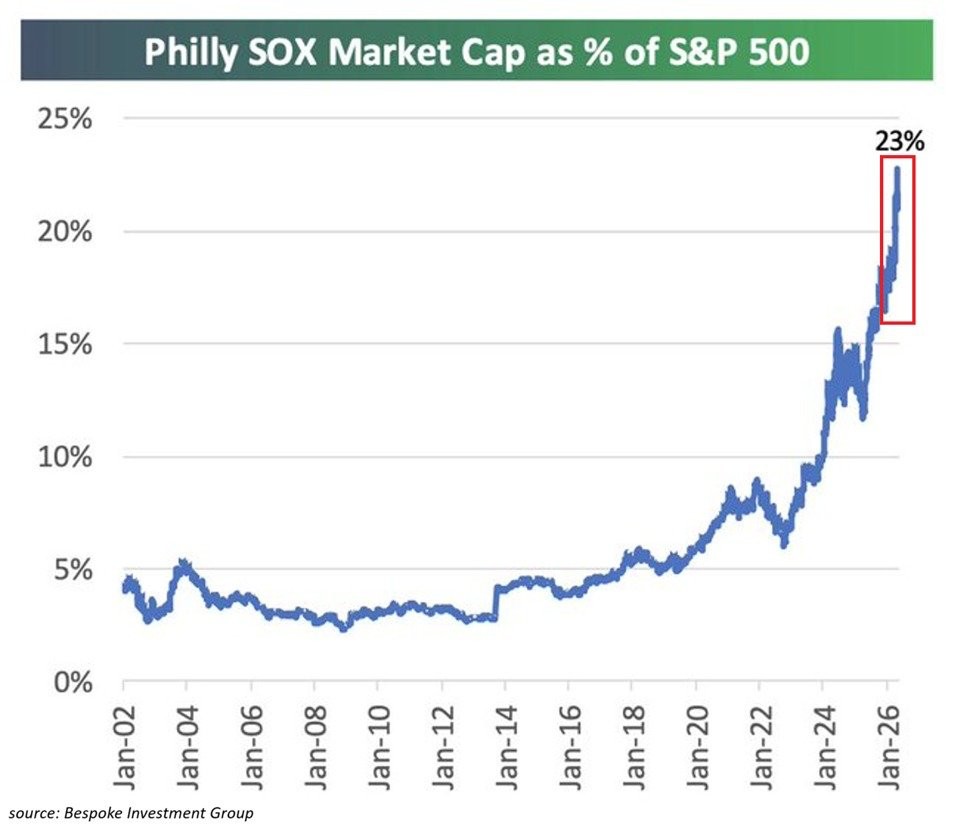

Building further on the previous charts showing rising AI concentration in the S&P 500, this chart highlights how semiconductors have become one of the biggest beneficiaries of the AI investment cycle. The market capitalization of the PHLX Semiconductor Sector Index has surged to nearly 23% of the S&P 500, reflecting the massive demand for AI chips, datacenters, cloud infrastructure, and high-performance computing systems. As AI adoption accelerates globally, semiconductor companies are seeing strong growth because they provide the essential hardware needed to train and run AI models.

In the current market environment, this explains why investors continue allocating capital aggressively toward chipmakers and AI infrastructure-related companies despite broader economic uncertainties. The rapid expansion of AI datacenters, cloud services, and enterprise AI deployment is creating a strong demand cycle for advanced semiconductors and networking systems. At the same time, the sharp rise in semiconductor weight within the broader market also shows how increasingly dependent market performance has become on continued AI spending momentum.

Conclusion

Overall, the charts show that the current market rally is becoming heavily dependent on AI-driven earnings growth, infrastructure spending, and a small group of large technology companies. Rising AI concentration in the S&P 500, along with aggressive EPS growth expectations, reflects strong optimism around the long-term AI cycle. However, this also increases market vulnerability, as any slowdown in AI spending, weaker monetization, or softer earnings delivery could create broader volatility and become a major hurdle for overall equity market performance.