This chart shows that global oil inventories are falling rapidly and could soon approach critically low operational levels if current supply disruptions continue. The recent decline accelerated after rising geopolitical tensions in the Middle East, particularly around the Iran–Israel conflict escalation, highlighting how dependent global energy markets remain on the region. Inventories act as a safety buffer for the oil market, and when they fall too low, the system becomes much more vulnerable to supply shocks, shipping disruptions, or unexpected demand spikes.

The projection suggests inventories could move below operational stress levels and even near the minimum threshold required for smooth refinery and pipeline operations. In the current market environment, this is concerning because tighter oil supplies can quickly push crude prices higher, feeding into transportation, manufacturing, and food costs globally. That raises the risk of another inflationary cycle at a time when central banks are already struggling to balance inflation control with slowing growth.

When viewed with the previous chart, this data shows that the global oil market is tightening much faster than normal. Although inventories started 2026 at relatively comfortable levels, the sharp projected decline indicates that supply-demand pressures are intensifying quickly. Compared with previous years, the 2026 trajectory stands out as unusually weak, suggesting that the market is struggling to rebuild inventories amid ongoing geopolitical and supply-side uncertainties.

This is concerning because lower inventories reduce the market’s ability to absorb disruptions such as production outages, shipping issues, or further escalation in Middle East tensions. As supply buffers shrink, oil prices become more sensitive to even small shocks, increasing the risk of higher volatility in energy markets. In the near term, if current conditions persist, it could lead to further supply stress, upward pressure on crude prices, and renewed inflation concerns across the global economy.

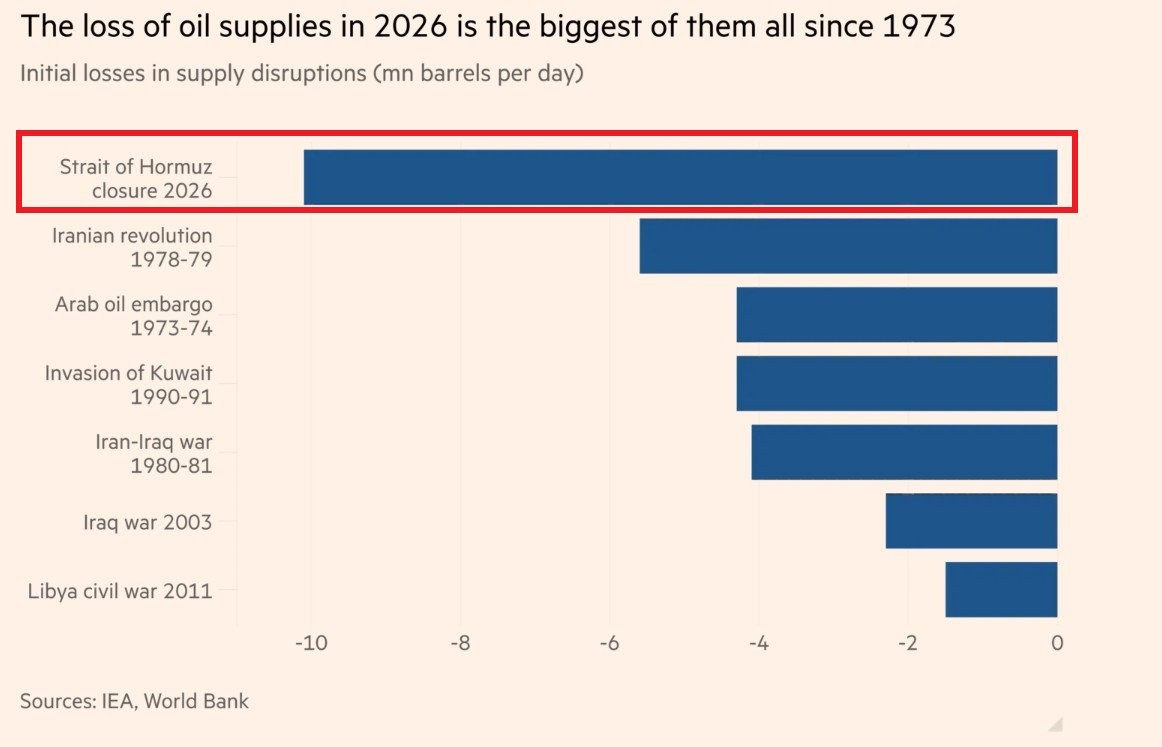

When correlated with the previous two charts, this data shows that the current oil shock is becoming one of the largest supply disruptions in modern history. A potential Strait of Hormuz closure in 2026 could remove more oil supply from the market than major past crises such as the 1973 oil crisis or the Iranian Revolution, while global oil inventories are already declining rapidly and supply buffers are weakening. This leaves the market far less prepared to absorb another major disruption. The concern is not only the immediate rise in crude prices, but also the possibility of a prolonged recovery period, as oil prices were already elevated before the disruption risk intensified. Highly energy-dependent economies could face severe inflationary pressure through higher fuel, transport, and import costs, increasing the risk of weaker demand, slower growth momentum, and broader economic instability. Overall, the charts together suggest the global economy may be entering a deeper energy stress cycle where tightening inventories, geopolitical tensions, and historically large supply disruptions could sustain inflation and volatility for an extended period.

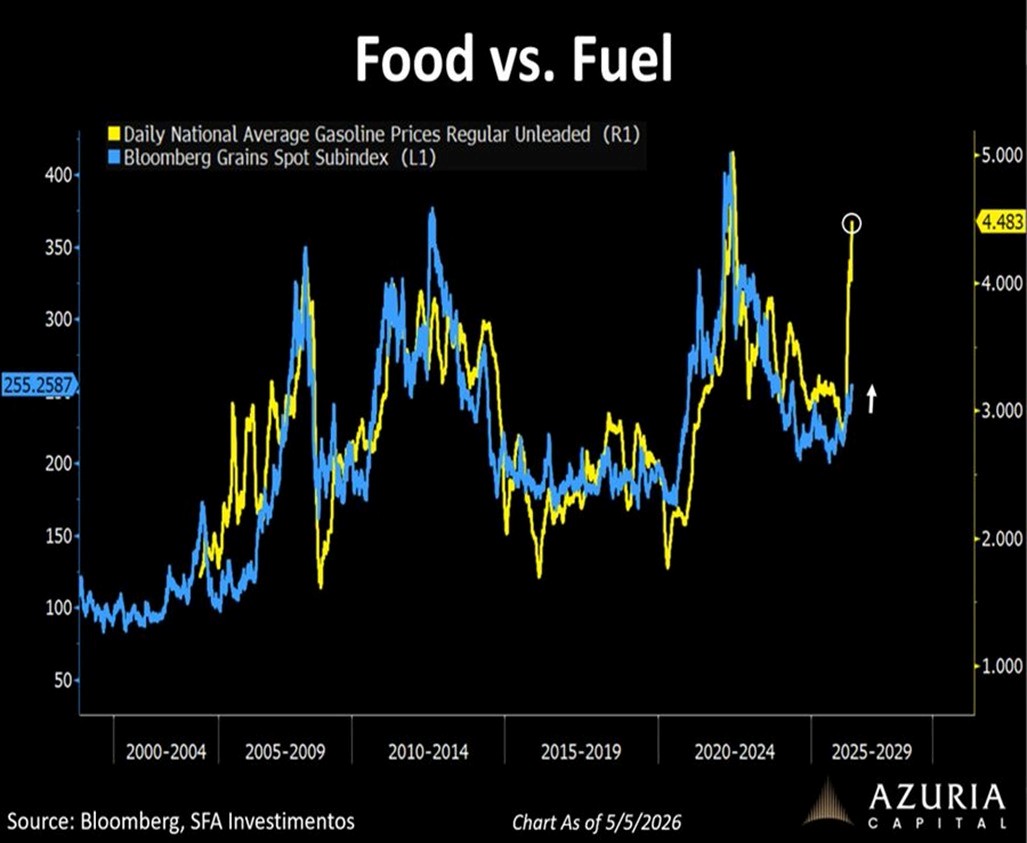

When linked with the previous oil inventory and supply disruption charts, this data highlights the strong connection between fuel and food inflation during periods of energy stress. The chart shows that when gasoline prices rise sharply, grain prices often follow, reflecting how dependent the global food system is on energy for transportation, fertilizers, and logistics. With oil markets already under pressure from falling inventories and geopolitical tensions around the Strait of Hormuz, the recent spike in fuel prices increases the likelihood of renewed food inflation in the near term.

This concerns the current macro environment because inflation is increasingly being driven by supply disruptions rather than strong demand. Rising fuel costs push up agricultural and distribution expenses, which eventually feed into consumer food prices and broader living costs. For energy-importing economies, this creates additional pressure through higher import bills and weaker purchasing power.

Overall, the chart suggests that the ongoing oil shock could spread beyond energy markets into a wider inflation cycle, increasing the risk of persistent inflation, slower growth, and continued economic uncertainty globally.

Conclusion

The broader implication is that the global economy is becoming increasingly vulnerable to energy-related shocks at a time when financial conditions and growth momentum are already fragile. With supply resilience weakening and geopolitical risks remaining elevated, the margin for stability is narrowing significantly. This environment raises the probability of longer-lasting inflation cycles, tighter policy constraints, and more frequent disruptions across global markets, making the path toward stable and sustainable economic growth far more challenging in the coming years.