Market Corrections Create Opportunity, Not Fear

The chart shows that the valuation premium of MSCI India Index over both the MSCI All Country World Index and MSCI Emerging Markets Index had expanded significantly in past years, reflecting strong growth expectations and heavy investor positioning toward India. However, the recent moderation in both trailing and forward P/E spreads means that this excess premium has cooled significantly, even as the broader earnings outlook remains stable. This compression suggests that valuations are now aligning more closely with fundamentals rather than sentiment-driven expansion, reducing downside risk from multiple contractions. As a result, the current phase reflects a more balanced entry point where the structural growth story remains intact while pricing has become relatively more reasonable, making Indian equities increasingly attractive from a risk-reward perspective.

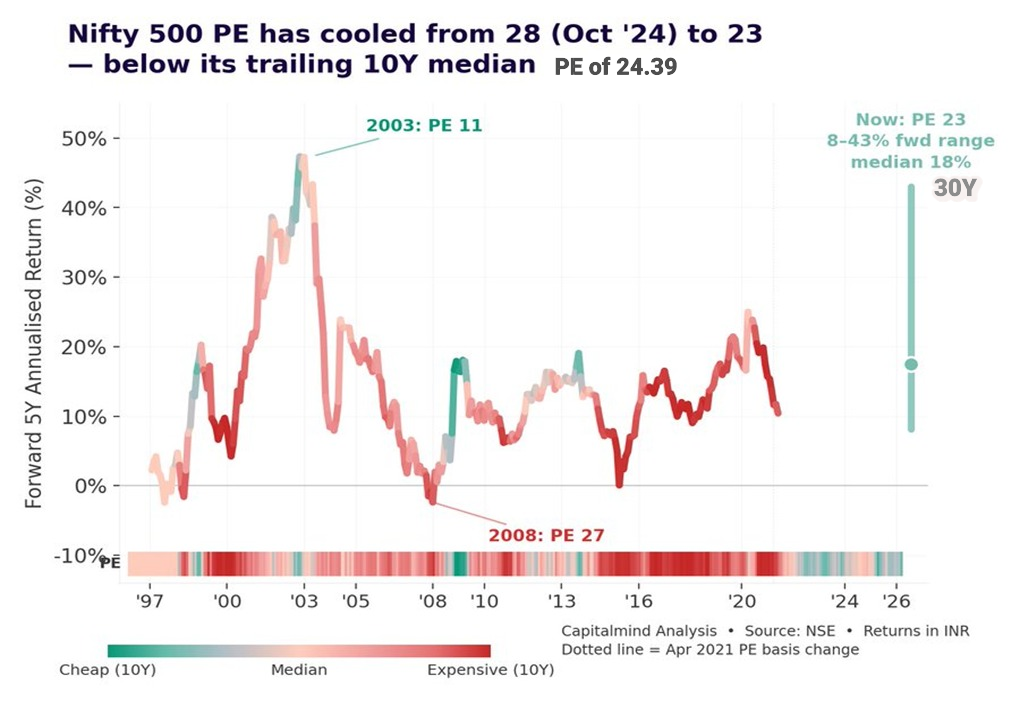

The chart highlights a meaningful valuation reset in the Nifty 500, with the PE cooling from elevated levels of 28 to around 23 over the past 18 months. Historically, this shift is important because starting valuations have largely influenced the downside risk rather than limiting upside potential. Periods marked in green (lower PE zones) consistently delivered strong forward returns of 15%+, while even higher valuation phases (red zones) still produced a wide range of outcomes, often remaining positive.

What this implies in the current context is that the market has moved out of an expensive zone into a more balanced-to-attractive valuation band, reducing the risk of sharp drawdowns. With earnings growth intact and valuations no longer stretched, the risk-reward is now tilted more favorably.

The compression in valuations has created a healthier entry point, suggesting that over the next few years, returns are likely to normalize on the upside, making the current phase a constructive accumulation zone rather than a cautionary one.

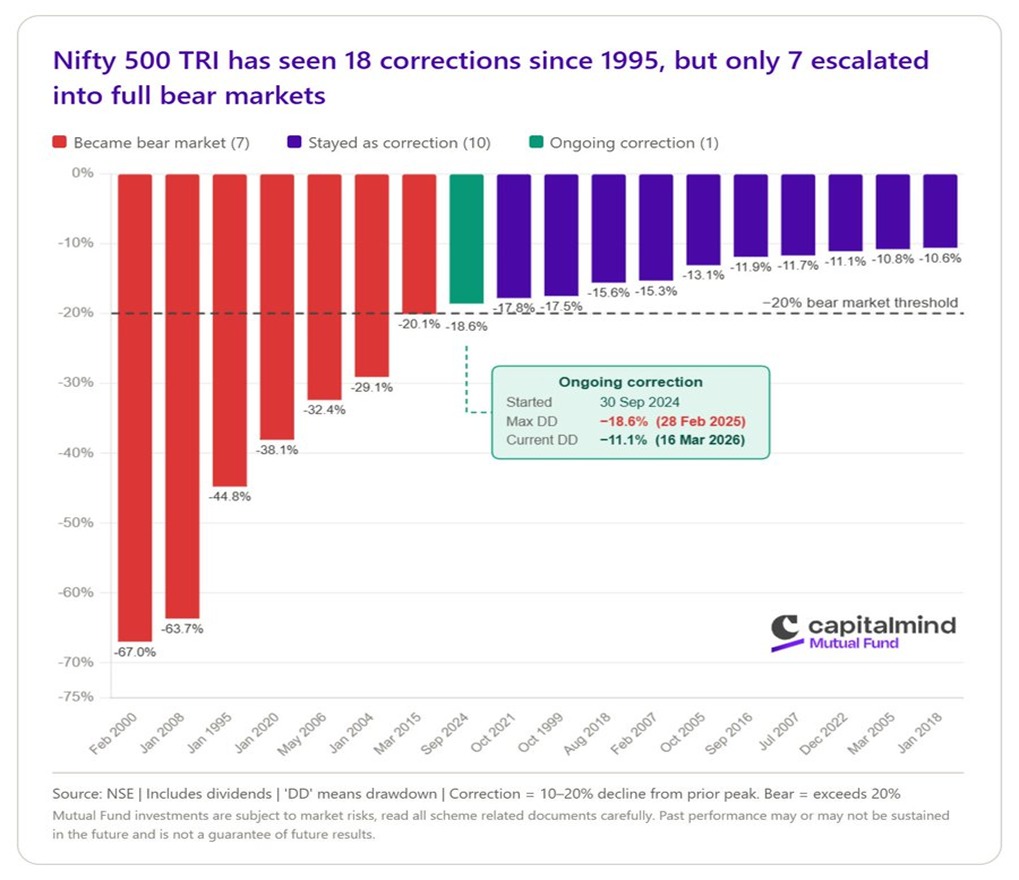

The broader picture across all charts suggests that the recent weakness in the Nifty 50s is part of a normal correction phase rather than a structural bear market. Historically, assuming a bear market is defined by a -20% decline, current levels remain comfortably above that threshold—even at the recent lows. In fact, more than half of past 10–20% corrections have not escalated into full bear markets, though the current drawdown stands among the closer calls.

At the same time, this correction has helped normalize the premium of the MSCI India Index, while consistent domestic flows have kept the market resilient despite global uncertainty and geopolitical noise. This reinforces the idea that such volatility is often temporary unless accompanied by deeper macro stress.

Overall, the combination of historical correction behavior, improving valuations, and strong domestic participation suggests that the market is undergoing a healthy reset, where near-term volatility may persist but reflects a transition toward more sustainable and broad-based growth, setting the stage for improved market stability and stronger earnings visibility in the coming phases.

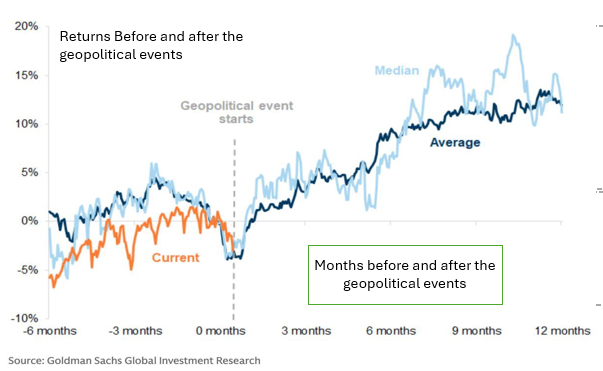

When this chart is viewed alongside the previous correction data of the Nifty 500 TRI, a consistent pattern becomes clear markets tend to react negatively in the immediate aftermath of geopolitical events, but these declines are typically short-lived and followed by recovery phases. The current trend (orange line) shows a similar initial dip, aligning with historical behavior where uncertainty drives temporary weakness.

Importantly, past data indicates that after such events, markets not only stabilize but gradually move higher over the following months, often making new highs as clarity returns and risk appetite improves. When combined with the fact that most corrections do not turn into full bear markets, this reinforces the idea that such phases are driven more by sentiment than structural damage.

Overall, the current setup suggests that this dip is more of a temporary dislocation rather than a long-term trend reversal, making it a strategic opportunity to deploy capital gradually, as history shows markets tend to recover and create wealth once the uncertainty phase passes.

The chart shows that India’s share in global market capitalization has fallen to around ~3%, marking a decline from earlier highs and indicating a shift in global investor allocation. When seen in the context of earlier trends like valuation normalization and evolving financial conditions, this suggests that capital is moving away from previously crowded positions and becoming more selective.

This decline does not point to structural weakness but rather reflects a rebalancing phase after a period of strong outperformance. As excess positioning gets unwound and market participation becomes more balanced, the focus is gradually shifting toward fundamentals like earnings and stability. Overall, this phase signals a transition in market dynamics, where future performance will likely be driven more by sustainable growth rather than liquidity-driven expansion.

Conclusion:

The current phase reflects a transition where uncertainty is being absorbed without materially altering the broader market cycle. As clarity improves, capital tends to shift back toward risk assets, creating a supportive backdrop for equities. This environment often rewards early positioning, as markets typically move ahead of visible improvements in data.

Additionally, with volatility already priced in, the probability of sharp downside reduces unless triggered by a major macro disruption, while the upside can gradually build as confidence returns. Sectoral participation is also likely to broaden, supporting a more sustainable move rather than a narrow rally.

Overall, the present setup favors a measured and phased increase in equity exposure, where positioning during uncertainty can potentially benefit from improving sentiment, liquidity shifts, and the next leg of market expansion.

Comments are closed.