Oil Shock. Equity Fear. Buying Opportunity.

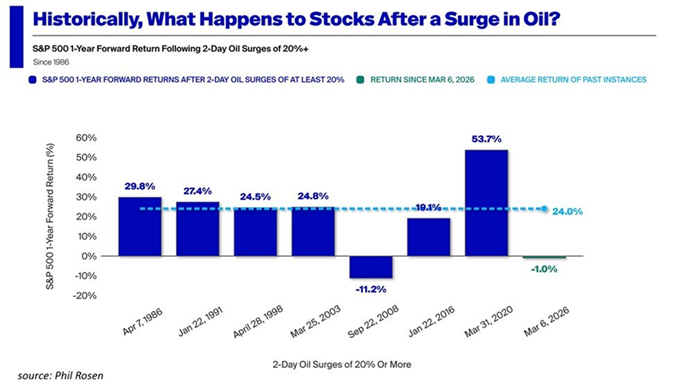

Sharp oil spikes have historically created an immediate risk-off reaction in equities, but they have not usually marked the start of a long-lasting bear market on their own. In most of the past cases shown in the chart, the S&P 500 was higher over the following 12 months, which suggests that markets tend to recover once the initial fear of energy costs, inflation pressure, and growth disruption begins to ease. The strongest recoveries came in periods when the oil surge was seen as temporary and the broader economy remained resilient enough to avoid a deep downturn. The clear exception was 2008, when the oil shock occurred alongside a full-blown financial crisis, causing equities to fall much further because the problem was not just higher oil, but a collapse in the underlying macro environment. So, the broader takeaway is that oil shocks should be viewed less as a standalone bearish signal and more as a test of macro strength. If the spike does not lead to prolonged inflation, aggressive central bank tightening, or recession, equities have historically treated that volatility as a buying opportunity.

Conclusion

A sharp rise in crude and oil prices often creates a temporary shock in equities, as higher energy costs quickly pressure sentiment and trigger near-term volatility. But unless that spike develops into a broader economic crisis, such corrections have historically been short-lived rather than structural. That is why oil-driven equity weakness should be seen more as a dislocation than a lasting breakdown. For long-term investors, phases of panic linked to sudden oil spikes have often provided attractive accumulation opportunities, as market fear tends to overshoot while the broader investment cycle remains intact.

Macro implication:

The broader implication is that a sudden surge in oil prices mainly acts as a transmission channel into inflation expectations, corporate cost pressures, and short-term risk aversion, but its longer-term market impact depends on whether it changes the direction of the business cycle. If growth, liquidity, and policy flexibility remain intact, the shock tends to fade, and capital rotates back into risk assets. We believe that the crude oil may have already peaked when it reached 120 levels. We believe that global equities are well positioned for a near-term rally over the next 2 months. We expect US and India to lead the rally this time around. S&P 500 could retest its all-time highs by May and NIFTY could go all the way to 26K plus over the same time frame.

Comments are closed.