The Great Imbalance: Rising Debt, Slowing Economic Momentum

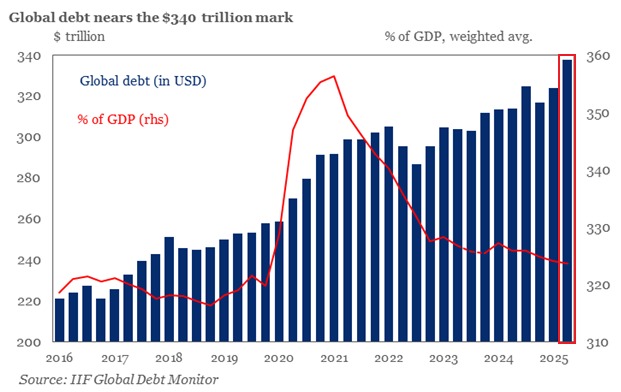

The chart highlights a critical shift in the global macro landscape: while absolute global debt has continued to climb relentlessly—now approaching ~$340 trillion—the debt-to-GDP ratio (red line) has stopped rising and is gradually easing from its pandemic peak. This divergence signals that economic growth has resumed but is not strong enough to offset the sheer scale of accumulated leverage. The concern for markets is that this elevated debt base leaves economies highly sensitive to interest rates, refinancing risks, and adverse liquidity conditions. In the current environment of tighter monetary policy, persistent inflation uncertainty, and fragmented global growth, even small rate shocks can amplify stress across sovereigns and corporates. Geopolitically, ongoing tensions are further pushing governments toward higher fiscal spending—defense, subsidies, and supply-chain restructuring, making debt structurally sticky. For markets, this creates a fragile equilibrium: liquidity-driven rallies can continue in the near term, but the long-term backdrop remains constrained by high leverage, limiting central banks’ flexibility and increasing the probability that future shocks, whether economic or geopolitical—translate into sharper volatility and periodic risk-off phases.

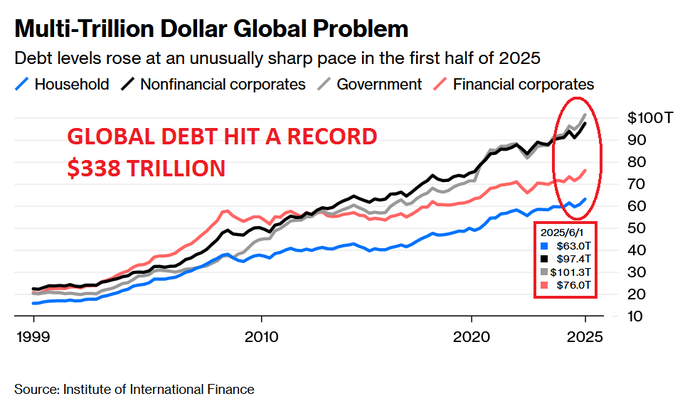

When viewed alongside the previous chart, this shows that the rise in global debt is not only large but spread across all major sectors. Government debt is increasing due to continued fiscal deficits and geopolitical spending, while non-financial corporates are borrowing more to cope with higher costs and weaker demand. At the same time, financial sector leverage is rising amid tighter liquidity, and household debt is growing as consumption becomes more credit-driven in a high-rate environment. This broad-based increase indicates that global growth is relying more on borrowing rather than strong underlying demand. In the current market scenario—where inflation remains relatively sticky and central banks are cautious about rate cuts—this creates a fragile balance. Higher rates put pressure on borrowers, while early easing risks reigniting inflation. As a result, growth visibility remains uncertain, with markets likely to swing between liquidity-driven optimism and periods of volatility due to rising debt servicing and refinancing risks.

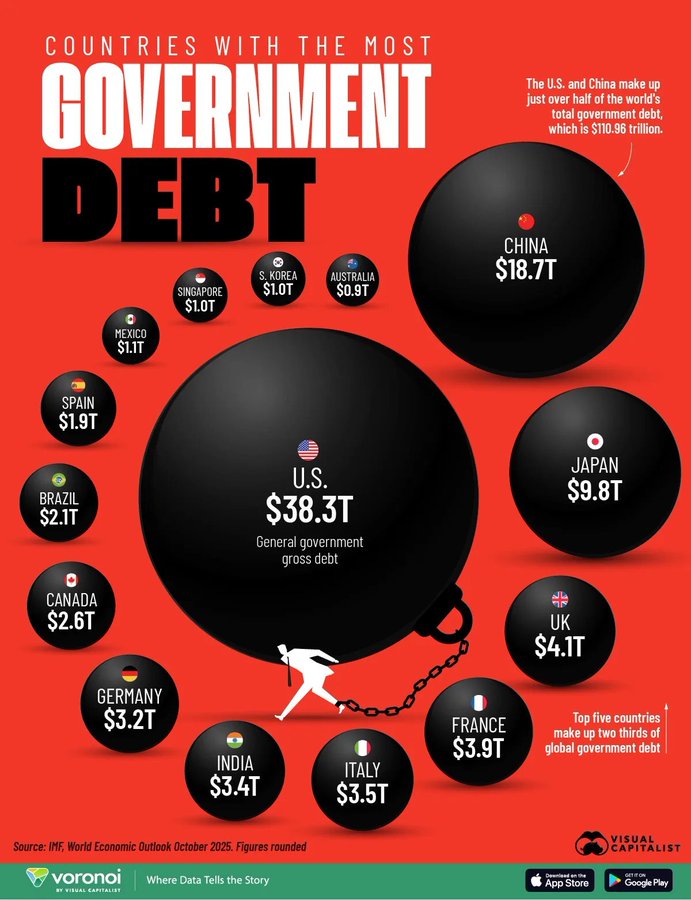

The U.S. continues to expand debt through persistent fiscal deficits and global reserve currency privileges, while China’s rising debt reflects its growth model driven by infrastructure, property, and state-led financing. This creates a structural vulnerability for the global economy: any slowdown in U.S. consumption or instability in China’s growth engine can have outsized ripple effects across trade, capital flows, and financial markets. Over the longer term, such heavy reliance on debt-funded growth from these two economies raises concerns about sustainability, limiting policy flexibility and increasing uncertainty around global growth stability.

Conclusion

The broader takeaway is that global stability is becoming increasingly dependent on how a few large economies manage their rising debt burdens, leaving the system with very little room for policy mistakes. As debt continues to grow faster than real economic productivity, it creates a structural drag where more resources are diverted toward interest payments rather than growth-generating investments. This weakens the effectiveness of traditional policy tools—fiscal stimulus adds to debt stress, while tighter monetary policy increases repayment pressure. Over time, this imbalance can lead to slower and more uneven global growth, higher sensitivity to interest rate changes, and frequent market disruptions. In such an environment, even small economic or geopolitical shocks can trigger larger ripple effects, making the overall macro landscape more fragile and prone to cycles of instability rather than sustained expansion.

Comments are closed.