From Gulf to Global: The Hidden Link Driving Food Inflation

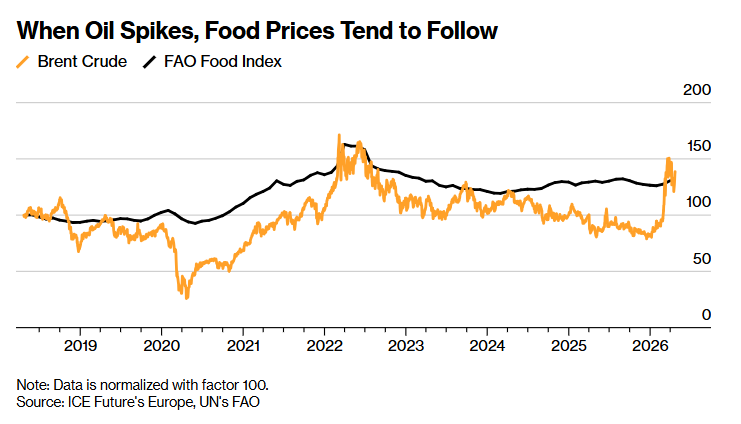

This chart highlights a strong relationship between oil prices and global food inflation—when crude oil rises, food prices tend to follow with a lag. The reason is structural: energy is a key input across the entire food supply chain, from fertilizers (which depend on natural gas), to transportation, processing, and storage. When oil spikes, these input costs rise, eventually pushing up the global food index. This was clearly visible during the 2021–2022 surge, and the recent uptick again suggests renewed upward pressure.

In the current scenario, this linkage is particularly important because geopolitical tensions, supply disruptions, and production controls are keeping energy markets volatile. As oil moves higher, it risks reducing food inflation globally, especially in import-dependent economies. This creates a second-round inflation effect, where higher food prices impact household budgets and keep overall inflation sticky. For central banks, this complicates the policy outlook, as easing rates become harder when essential inflation remains elevated.

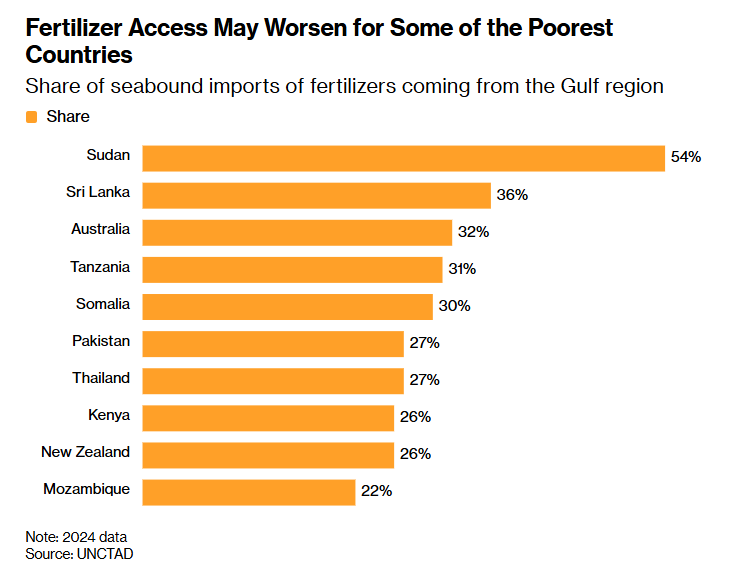

When this chart is linked with the earlier oil–food relationship, it highlights a deeper layer of risk coming from supply chain dependency. Many countries—such as Sudan, Sri Lanka, and Pakistan—rely heavily on fertilizer imports from the Gulf region, making them highly exposed to disruptions in energy-rich export hubs. Since fertilizer production is closely tied to energy inputs, any volatility in oil and gas markets or geopolitical tensions in the Gulf can directly restrict supply or increase costs. This creates a compounding effect: constrained fertilizer access reduces agricultural output, which then amplifies food price pressures already influenced by rising energy costs. In the current global environment—marked by fragile supply chains, trade uncertainties, and regional conflicts, this dependency increases vulnerability for import-reliant economies, particularly those with limited fiscal capacity. The result is a heightened risk of food insecurity, inflation persistence, and uneven global growth, where shocks in one region quickly cascade into broader economic stress.

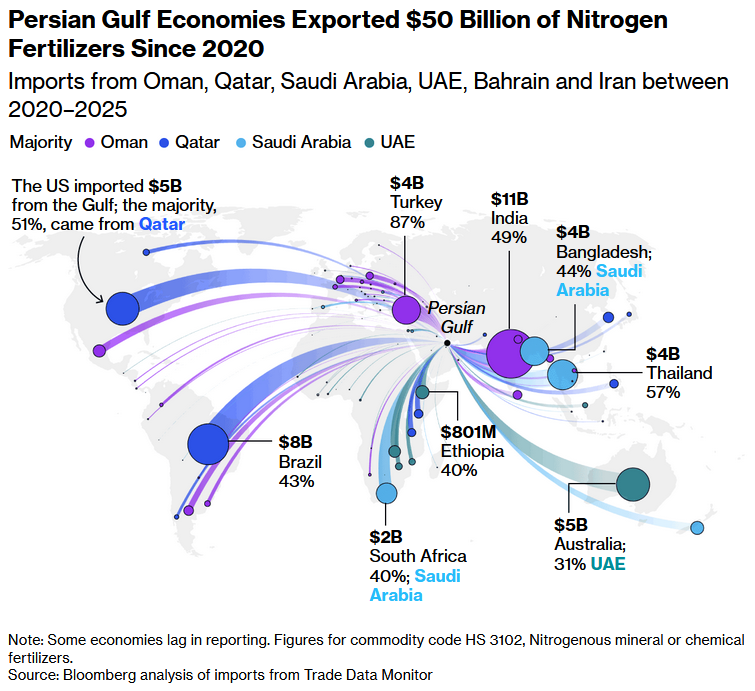

When this chart relates to the previous one, it clearly shows how deeply the global food chain is tied to the Persian Gulf for fertilizer supply. Major importers like India, Brazil, United States, and Bangladesh depend significantly on nitrogen fertilizer flows from countries such as Qatar, Saudi Arabia, and United Arab Emirates. This creates a critical chokepoint: any disruption—whether from geopolitical tensions, energy price spikes, or supply restrictions in the Gulf—can quickly tighten global fertilizer availability.

Linking this with the earlier oil–food dynamic, the risk becomes more pronounced. Higher energy prices or instability in the Middle East can simultaneously increase fertilizer costs and limit supply, reducing agricultural output across highly dependent economies. This leads to a cascading effect where food production declines just as input costs rise, pushing food prices higher. Countries with high import reliance and limited domestic buffers are especially vulnerable, as they face both cost inflation and supply shortages at the same time.

Conclusion

The heavy dependence on Gulf fertilizer exports creates a structural inflation risky disruption in the region can transmit directly into global food systems, amplifying inflation pressures in exposed economies and making food security and price stability increasing uncertain. This vulnerability is intensified by the concentration of supply routes and limited alternatives, meaning even short-term shocks can have outsized global effects. In the current environment of geopolitical tensions and volatile energy markets, this setup increases the likelihood of supply-driven inflation cycles, where costs rise not due to demand strength but because of constrained inputs. Over time, this can weaken agricultural resilience, strain trade balances for import-dependent nations, and make inflation more persistent, ultimately adding pressure on global growth stability.

Comments are closed.