This Reset Is Building the Next Bull Run

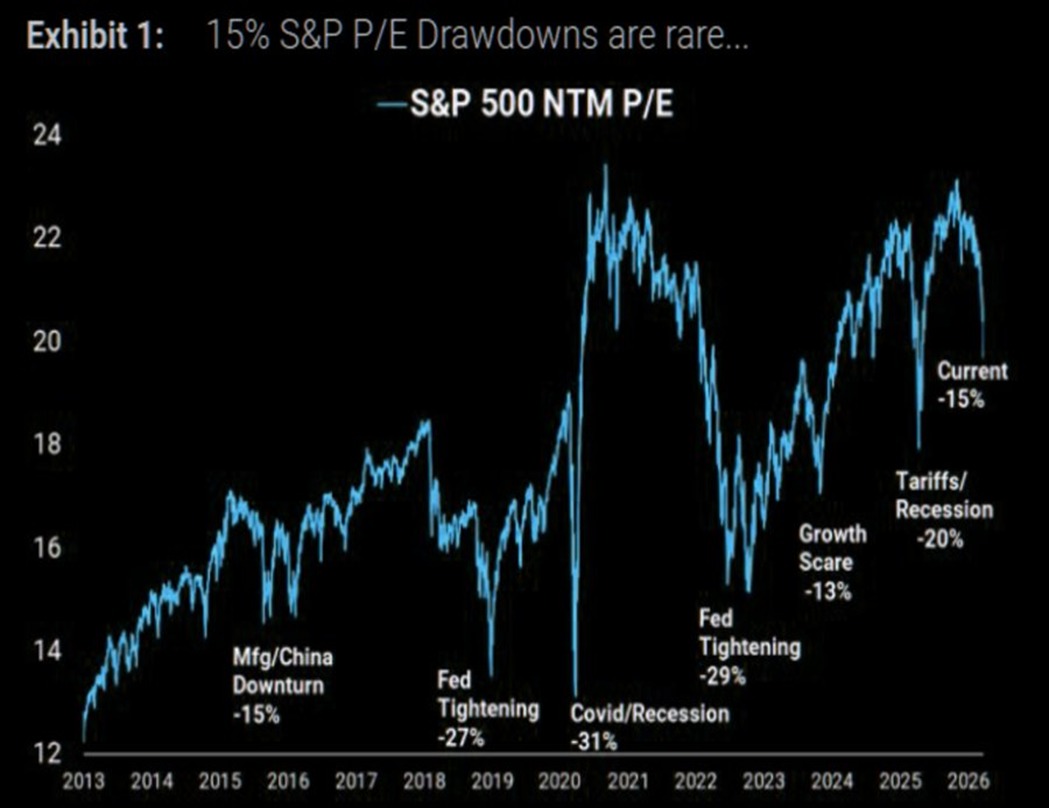

The chart indicates that the forward valuation of the S&P 500 has declined and is now hovering around its 5-year average P/E, after previously trading at elevated levels due to strong liquidity and optimism around growth sectors. This pullback reflects a meaningful correction in valuation rather than price alone, suggesting that excess premiums have been largely absorbed by the market.

In the current global backdrop—marked by tighter financial conditions, cautious central banks, and shifting capital flows—this normalization signals a transition toward a more sustainable phase where markets rely less on multiple expansion and more on underlying earnings strength. The recent dip toward the average also highlights that downside risks from overvaluation have reduced significantly compared to earlier peaks.

Overall, with valuations now closer to historical norms and much of the froth already cleared, the S&P 500 appears to be in a more attractive and balanced zone, where performance going forward is likely to be steadier and supported by fundamentals following the sharp correction in valuation.

In the medium term, the recent ~15% valuation drawdown in the S&P 500 aligns with past correction phases that typically occurred during periods of macro tightening or growth uncertainty. Such de-rating cycles are a normal part of market behavior, helping reset excess valuations built during liquidity-driven rallies.

With the index now trading closer to its historical average P/E, much of the overvaluation has already been corrected. This reduces downside risk from further multiple compression and shifts the market toward a phase where returns are more likely to be driven by earnings stability rather than valuation expansion.

Overall, in the medium term, this setup suggests a more balanced and constructive outlook, where the market may move through consolidation but gradually stabilizes and positions itself for steady performance as macro pressures ease.

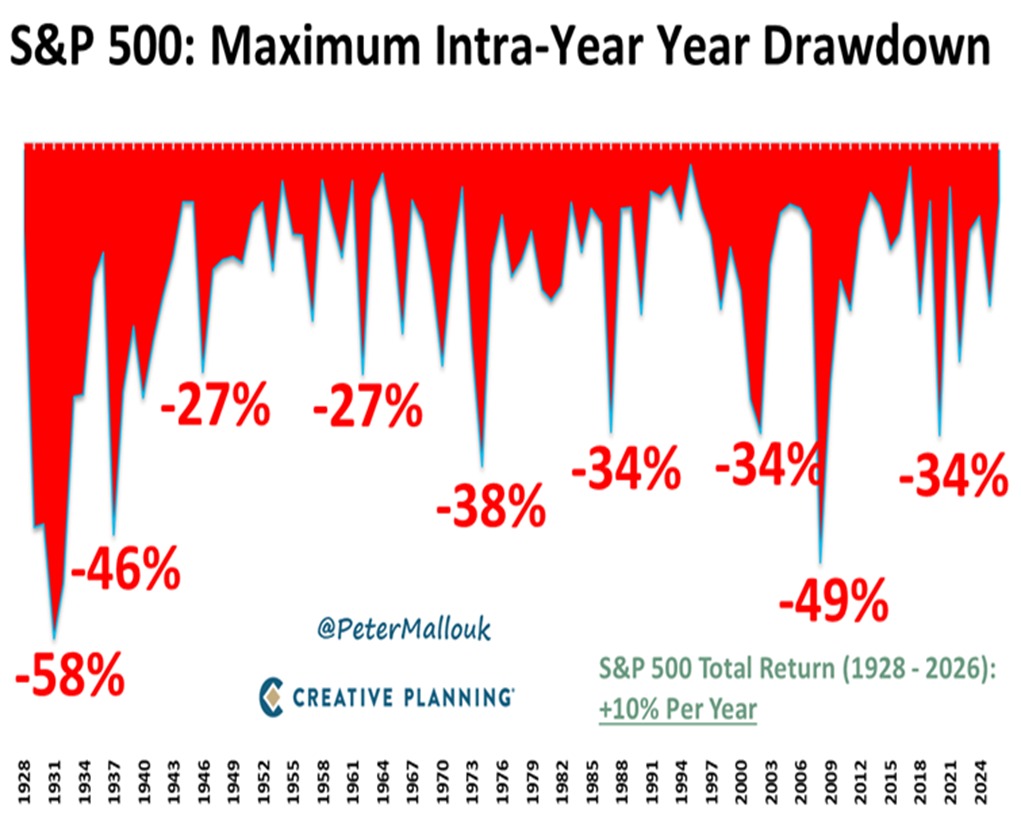

This chart shows that the S&P 500 has historically experienced frequent intra-year drawdowns of 10-20% yet still delivered strong long-term returns. When combined with the earlier insight of valuation correction bringing P/E back to its average, it reinforces that the current phase is a normal market reset, not a breakdown.

With both valuation compression and price correction already in place, much of the risk appears to be priced in. At the same time, the U.S. continues to hold an edge in terms of earnings strength and global capital preference, making it relatively more attractive compared to other markets.

Overall, this setup creates a bullish medium-term outlook, where the S&P 500 is well-positioned to outperform and potentially lead the next phase of global market recovery, with other markets likely to follow its direction.

Conclusion

Bringing it all together, the current environment reflects a market that has already absorbed multiple layers of stress and repositioning, leaving it structurally stronger rather than fragile. The reset in expectations, combined with resilient underlying fundamentals, places the S&P 500 in a position where future performance is less dependent on optimism and more grounded in actual growth delivery.

From here, the probability shifts toward a more durable and leadership-driven upcycle, where capital gravitates back to quality and consistency. Given the U.S. market’s dominance in innovation, earnings visibility, and global influence, it is well-placed to set the direction for broader global equity markets.

In essence, this phase appears to be a transition point toward the next leg of expansion, with the S&P 500 likely to emerge stronger and lead global equities into a more constructive and bullish cycle ahead.

Comments are closed.